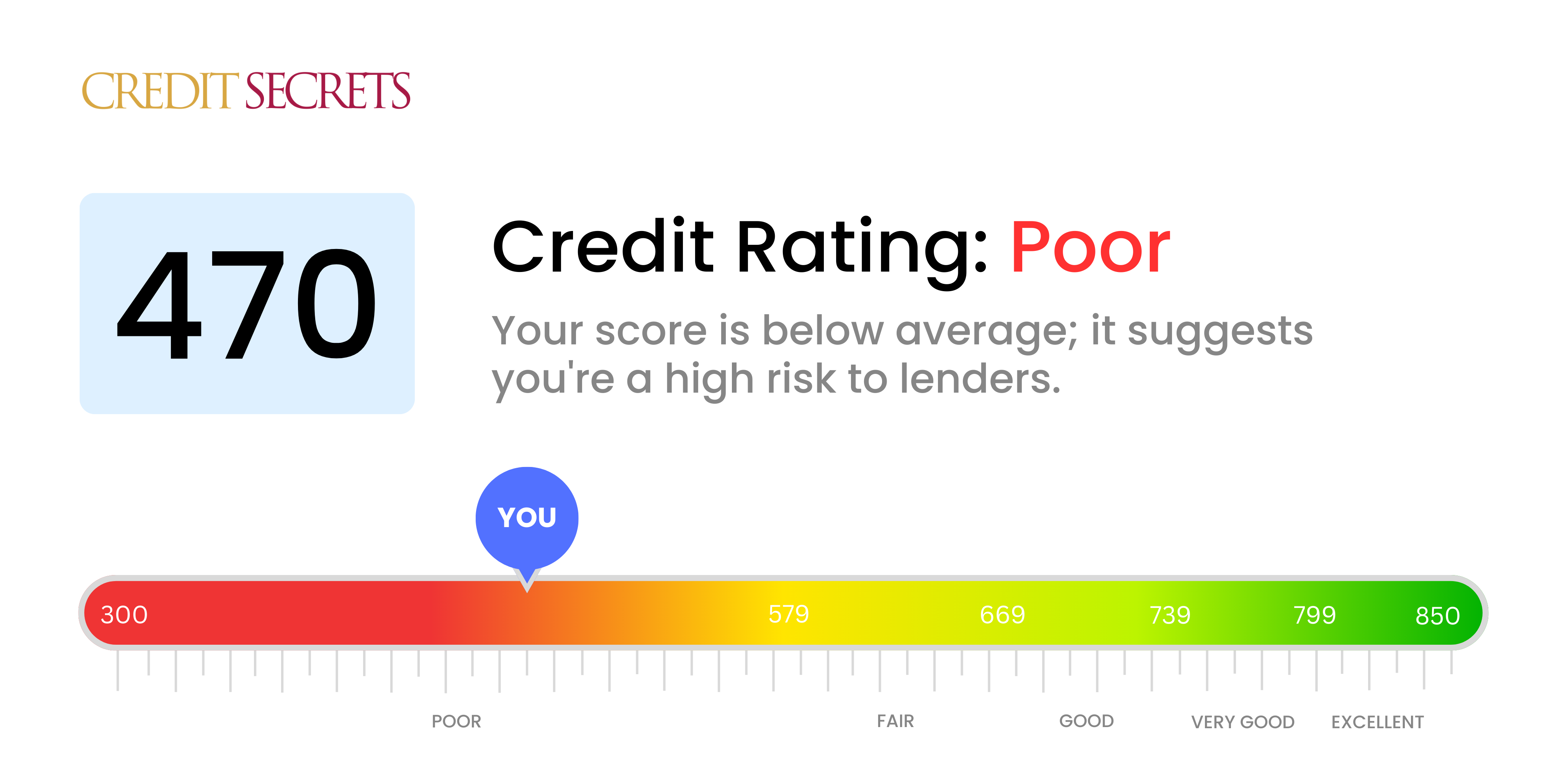

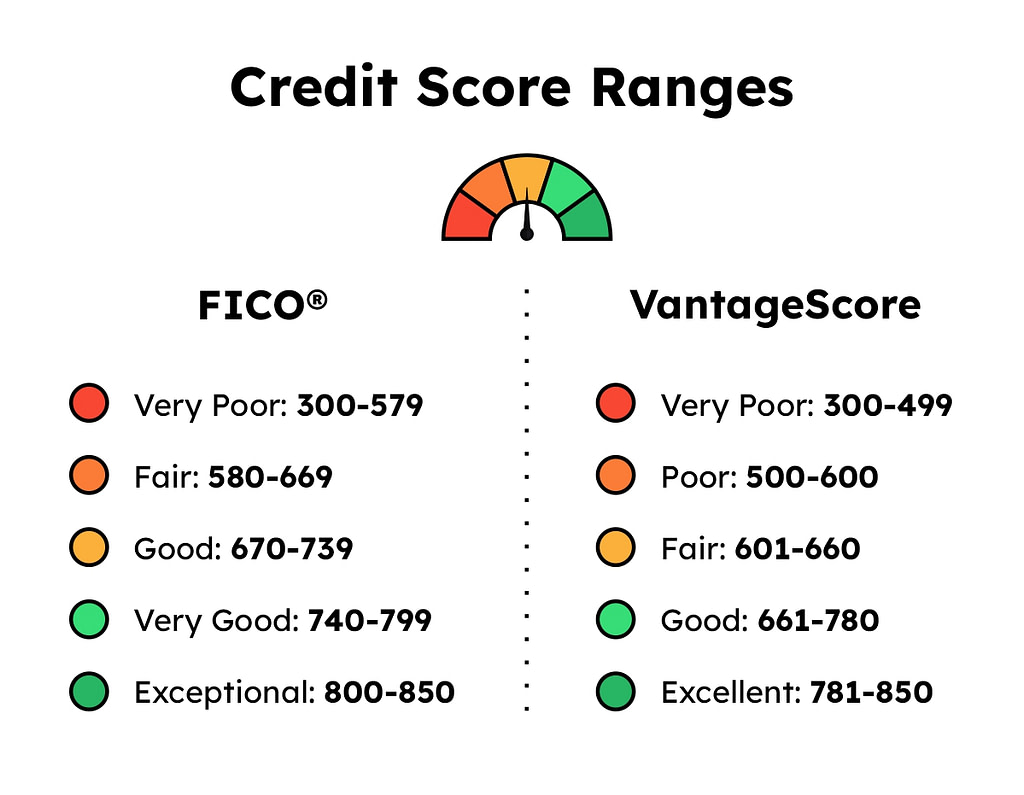

470 Credit Score Credit Card

Alright, friend, let's talk about something that might seem a little...intimidating. Credit scores. Specifically, credit scores in the 470 ballpark. Now, before you start picturing ominous music and locked doors, let's reframe this! A 470 credit score isn’t the end of the road; it's just a starting point.

And guess what? There are credit cards designed specifically for people in your shoes. Think of them as your trusty sidekick on your journey to financial awesomeness!

Why Even Bother with a Credit Card at 470?

Excellent question! (Seriously, you're asking all the right questions!) Even with a lower credit score, a credit card can be a powerful tool. It's not about racking up debt; it's about demonstrating responsible credit behavior.

Must Read

Think of it like this: you're showing lenders you can handle credit responsibly. You're building (or rebuilding) trust. And trust, my friend, is key to unlocking better interest rates on loans, mortgages, and even car insurance down the road. Plus, who doesn't love the convenience of swiping instead of carrying wads of cash?

Okay, So What Kind of Credit Cards Are We Talking About?

We're talking about secured credit cards and unsecured credit cards designed for people with less-than-perfect credit. Let’s break them down:

Secured Credit Cards: Imagine this as a "security deposit" for your credit card. You provide a cash deposit (usually matching your credit limit), and that deposit acts as collateral. If you don't pay your bill, the card issuer can use the deposit to cover the debt. But the magic happens when you do pay on time! Your responsible behavior gets reported to the credit bureaus, and your score starts to climb. It’s like leveling up in a video game!

Unsecured Credit Cards (for Fair/Bad Credit): These are a bit trickier to get with a lower score, but they exist! They don’t require a deposit. However, expect to see higher interest rates and potentially annual fees. The key here is to shop around and compare offers carefully. Don’t just grab the first card you see! (Unless it’s offering free tacos. Then, maybe grab it and compare later.)

What to Look For (and What to Avoid!)

When you're comparing credit card offers, keep these points in mind:

- Interest Rates (APRs): This is the cost of borrowing money. The lower the APR, the less you'll pay in interest. With a 470 credit score, expect higher APRs than someone with excellent credit. That's why paying your balance in full each month is crucial.

- Fees: Watch out for annual fees, monthly fees, late payment fees, and over-the-limit fees. These can eat into your available credit and make it harder to manage your finances.

- Reporting to Credit Bureaus: Make sure the card issuer reports your payment history to all three major credit bureaus (Equifax, Experian, and TransUnion). This is how you build credit!

- Credit Limit: Don’t expect a huge credit limit right away. Start small and use the card responsibly to prove you can handle more.

And what to avoid? Cards with ridiculously high fees, predatory lending practices, or confusing terms and conditions. If something seems too good to be true, it probably is!

Turning This Around: Strategies for Success

Getting a credit card is just the first step. The real magic happens when you use it wisely.

- Pay on Time, Every Time: Set up automatic payments so you never miss a due date. This is the single most important thing you can do to improve your credit score.

- Keep Your Balance Low: Aim to use no more than 30% of your available credit limit. This shows lenders you're not over-reliant on credit.

- Monitor Your Credit Report: Check your credit report regularly for errors or signs of fraud. You can get a free copy of your report from each of the three major credit bureaus once a year at AnnualCreditReport.com.

- Be Patient: Building credit takes time. Don't get discouraged if you don't see results overnight. Just keep making responsible choices, and you'll get there!

Remember, you're not just improving your credit score; you're building a foundation for a brighter financial future. That means better opportunities, more freedom, and less stress. And who doesn't want that?

So, ditch the fear, embrace the challenge, and get ready to take control of your credit. You've got this!

Feeling inspired? Fantastic! The next step is to research different credit card options and find one that fits your needs. There are tons of resources online to help you compare cards and learn more about credit management. Go forth and conquer your credit goals!