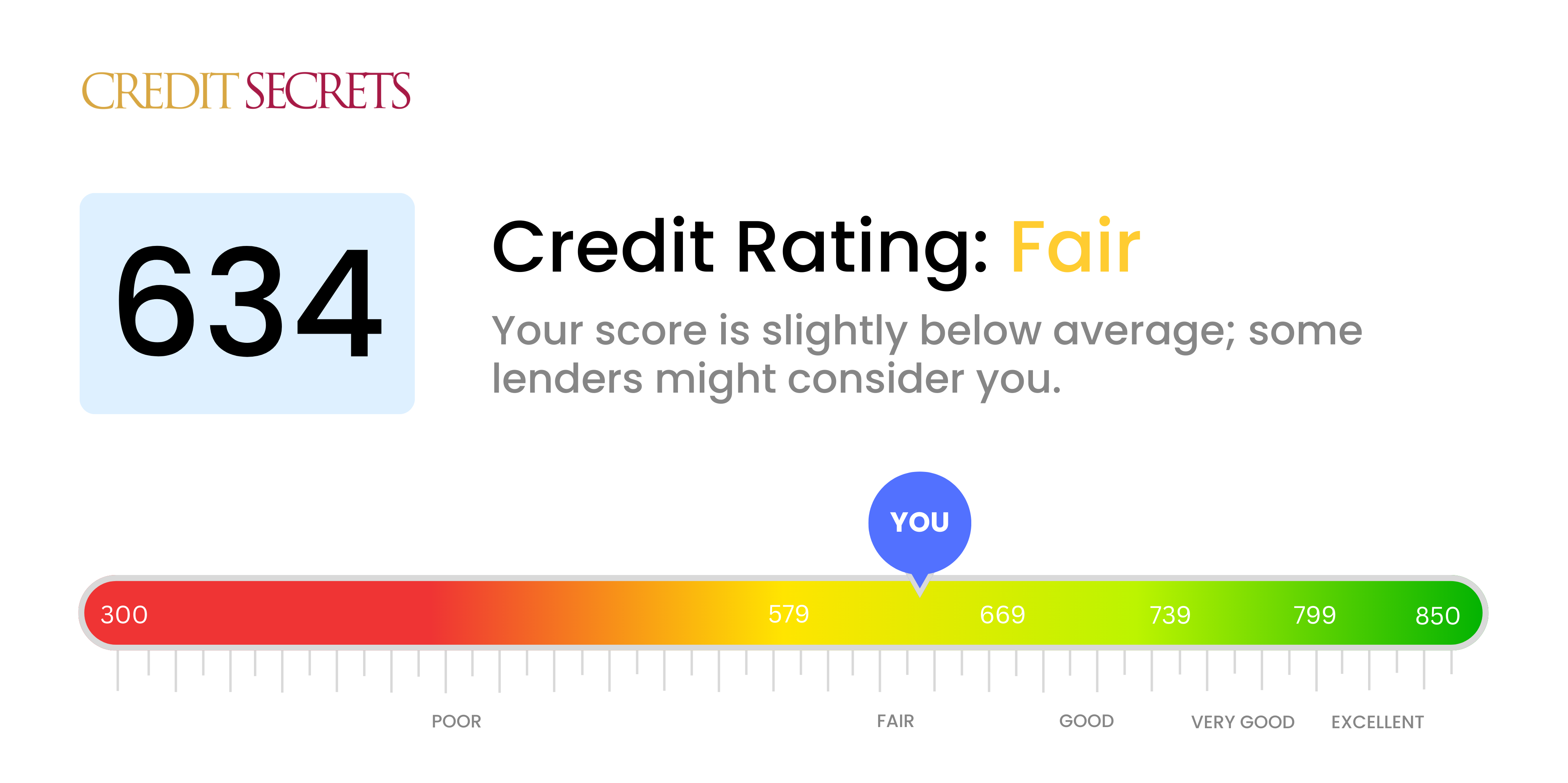

634 Credit Score Car Loan

Okay, let's talk about something nobody REALLY wants to talk about: car loans and that awkward three-digit number called your credit score. Specifically, the dreaded 634. It's not awful, but it's not exactly singing sweet nothings to the bank's loan officer, is it?

I have an unpopular opinion. Buckle up. I think the whole credit score system is a bit...dramatic. We’re all just trying to survive, right? A 634 is like a participation trophy in the adulting olympics. You showed up! You tried! Now, can you please just get a decent car without selling a kidney?

The 634 Credit Score Car Loan Adventure

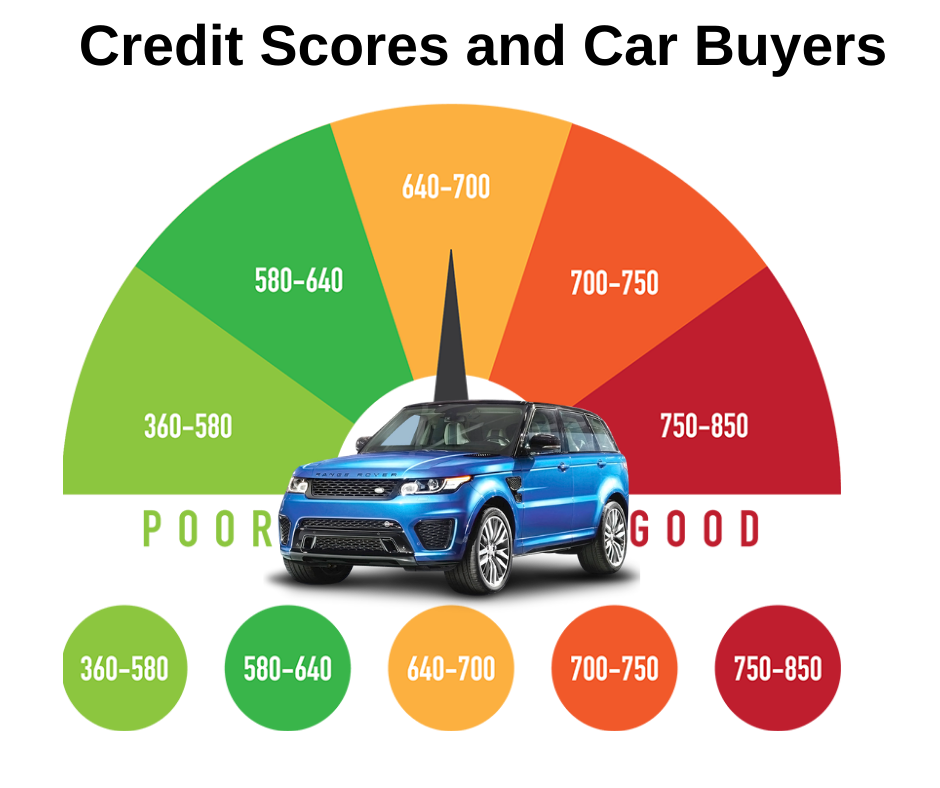

Getting a car loan with a 634 credit score can feel like navigating a jungle with a paper map. It’s possible, but you’re gonna encounter some interesting wildlife. Think high interest rates and loan terms longer than a Tolstoy novel.

Must Read

Let's be real. Those interest rates? Ouch. They can feel like you're paying for the car twice. You might hear things like, "Well, your credit isn't perfect..." as if you didn't already know! Trust me, I get it. I’ve been there. Eating ramen noodles while driving a “slightly used” car with an engine that sounded suspiciously like a lawnmower.

And the loan terms! Seven years to pay off a Honda Civic? That Civic will be practically antique by the time you own it outright. Your grandkids will be learning to drive in it. “Grandpa, what’s a CD player?”

The Down Payment Dance

Here's another thing: the down payment. With a 634, expect to put down more than just lint from your pockets. Think serious cash. The kind of cash you were secretly saving for that trip to Bora Bora. (Sorry, Bora Bora. Maybe next decade.)

Banks see a bigger down payment as a sign of good faith. It's like saying, "Hey, I'm serious about this car thing! See? I have money...ish." It lowers their risk, which means, in theory, a slightly less terrifying interest rate.

Unpopular Opinion #2: Shop Around!

This might sound obvious, but shop around. Like, really shop around. Don't just waltz into the first dealership you see and accept whatever they offer. That's like letting the first squirrel you meet pick your lottery numbers. Probably not the best strategy.

Check out credit unions, online lenders, and even those “we finance anyone!” dealerships (with a healthy dose of skepticism, of course). Get quotes from multiple places and compare the terms. Don’t be afraid to haggle! Channel your inner bargain hunter.

The Co-Signer Conspiracy (or Strategy)

A co-signer with a squeaky-clean credit score can be your knight in shining armor. Someone who’s willing to vouch for you and say, “Hey, I trust this person not to skip town with the car!” But be warned: a co-signer is a BIG ask. Make sure you’re reliable. Your relationship with that person is worth more than a shiny new SUV.

.png)

"With great co-signing power comes great responsibility." - Probably someone famous.

Building That Credit, One Payment at a Time

The good news? Every on-time car payment is a step towards improving your credit score. Think of it as climbing a mountain. Each payment is a step up. Eventually, you’ll reach the summit (aka a better credit score and lower interest rates). Then you can refinance and finally afford that Bora Bora trip. Maybe.

So, is getting a car loan with a 634 credit score fun? Nope. Is it possible? Absolutely. Just be prepared to do your homework, shop around, and maybe make a few ramen noodle sacrifices along the way. And remember, that 634 doesn’t define you. You’re more than just a number. You’re a driver with dreams of open roads and… affordable car payments.

And hey, at least you're not walking. That's a win in my book.