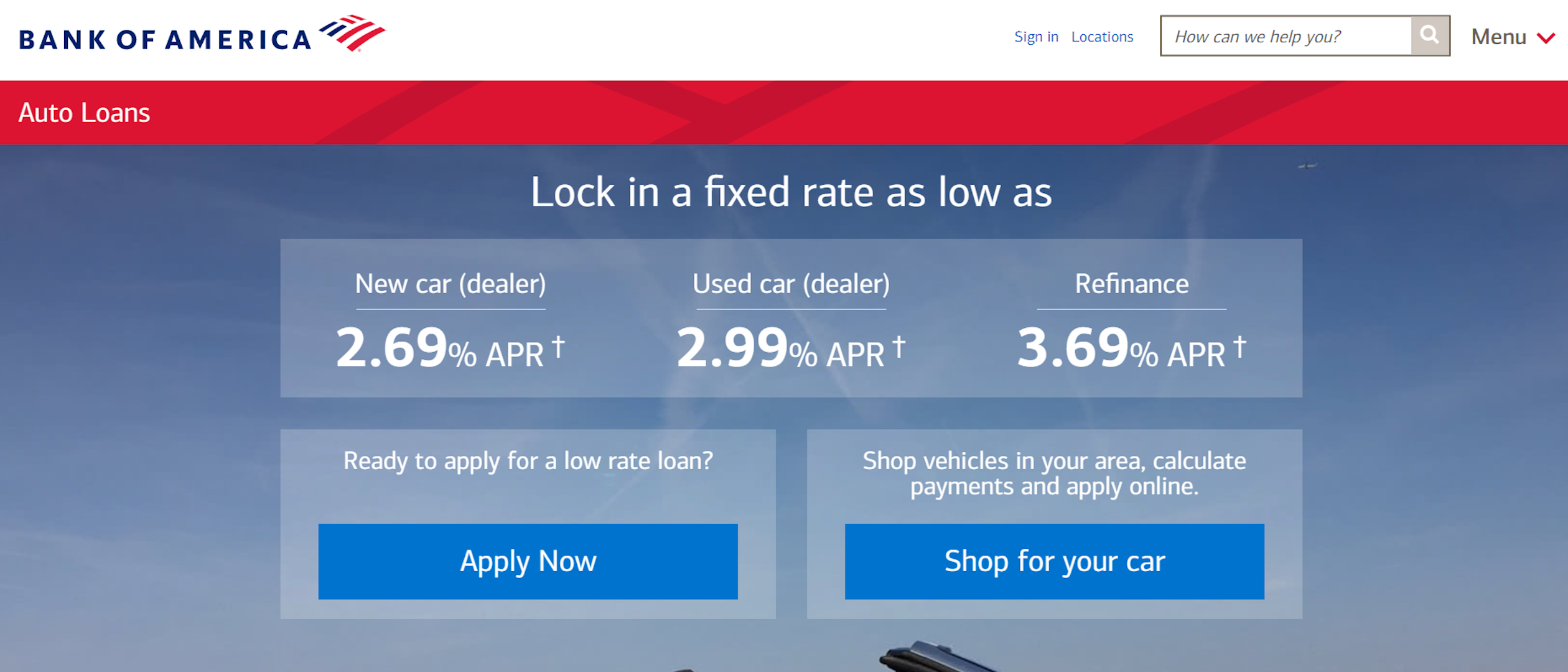

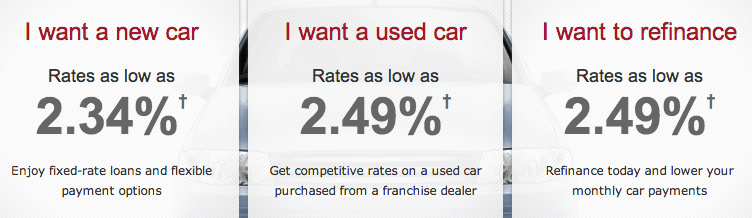

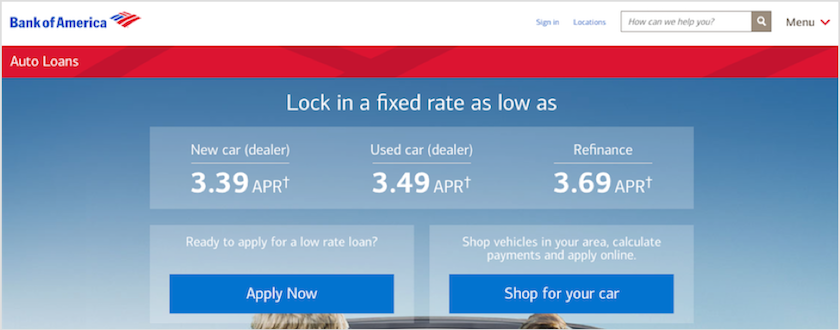

Bofa Auto Refinance Rates

Okay, so you're thinking about refinancing your car loan, huh? Smart move! Especially if you feel like you're throwing money away each month. And you're checking out Bank of America (BofA)? Not a bad starting point. But before you dive headfirst, let's chat about BofA auto refinance rates like we're grabbing coffee, alright?

First things first, remember those super low rates you see advertised? Yeah, those are usually for the most qualified borrowers. Like, perfect credit score, practically brand-new car, unicorn-riding levels of awesome. So, don't get discouraged if your rate isn't quite that low. We all start somewhere, right?

What actually impacts those BofA auto refinance rates? Buckle up, because it's a bit of a ride. Think of it like a recipe – lots of ingredients come into play.

Must Read

The Usual Suspects: Credit Score & History

Yep, your credit score is still king (or queen!). It’s the biggest influencer. A higher score generally means a lower interest rate. Banks love seeing that you're responsible with money, and a solid credit history proves it. Think of it as showing them you're not going to ghost them on payments. Nobody wants that! So, is your credit score looking spiffy? I sure hope so!

Pro Tip: Before you even think about applying, check your credit report! You can get it for free from AnnualCreditReport.com. Dispute any errors you find – even small mistakes can ding your score. Trust me, it's worth the effort. Plus, who doesn't love feeling like a financial detective?

Car Details: Age & Mileage Matter

Is your car a shiny new model or something a little... vintage? BofA, like most lenders, considers the age and mileage of your car. Older cars with high mileage are seen as riskier. It makes sense, right? They're more likely to need repairs. So a 2005 minivan with 200,000 miles might not get you the best rate. Sorry, minivan owners. We still love you.

Loan Term: Short & Sweet or Long & Lonely?

This is a big one! The loan term is the length of time you have to repay the loan. Shorter terms usually mean lower interest rates, but higher monthly payments. Longer terms mean lower monthly payments, but you'll end up paying more in interest over the life of the loan. It's a delicate balance, isn't it? Think about what works best for your budget. Can you handle a slightly higher payment to save money in the long run? Or do you need to keep those monthly bills as low as possible?

Loan Amount: How Much Are You Borrowing?

The amount you're refinancing also plays a role. A smaller loan amount might get you a slightly better rate than a larger one. But honestly, this isn't usually as impactful as your credit score or the car's age.

Bank of America Specifics: Are You Already a Customer?

Being a BofA customer can sometimes give you a slight advantage. They already know you and your banking habits. Think of it as like getting preferential treatment at your local coffee shop because you're a regular. They might offer you a slightly better rate as a loyalty perk. But don’t bank on it. (Pun intended!) It’s still important to shop around!

Okay, so what now? Don’t just accept the first rate you see from BofA (or anyone else, for that matter!). Shop around! Get quotes from multiple lenders – credit unions, online lenders, even your local bank. Comparison is key, my friend! It’s like dating, but with money. You want to find the best match.

And before you finalize anything, read the fine print! Seriously, I know it’s boring, but it’s crucial. Look for any hidden fees or penalties. You don’t want any nasty surprises down the road.

So, are BofA auto refinance rates worth it? It depends! Do your homework, compare offers, and choose what's best for your financial situation. Good luck! And hey, maybe we can grab coffee again and you can tell me all about your refinancing success. I'll bring the biscotti.