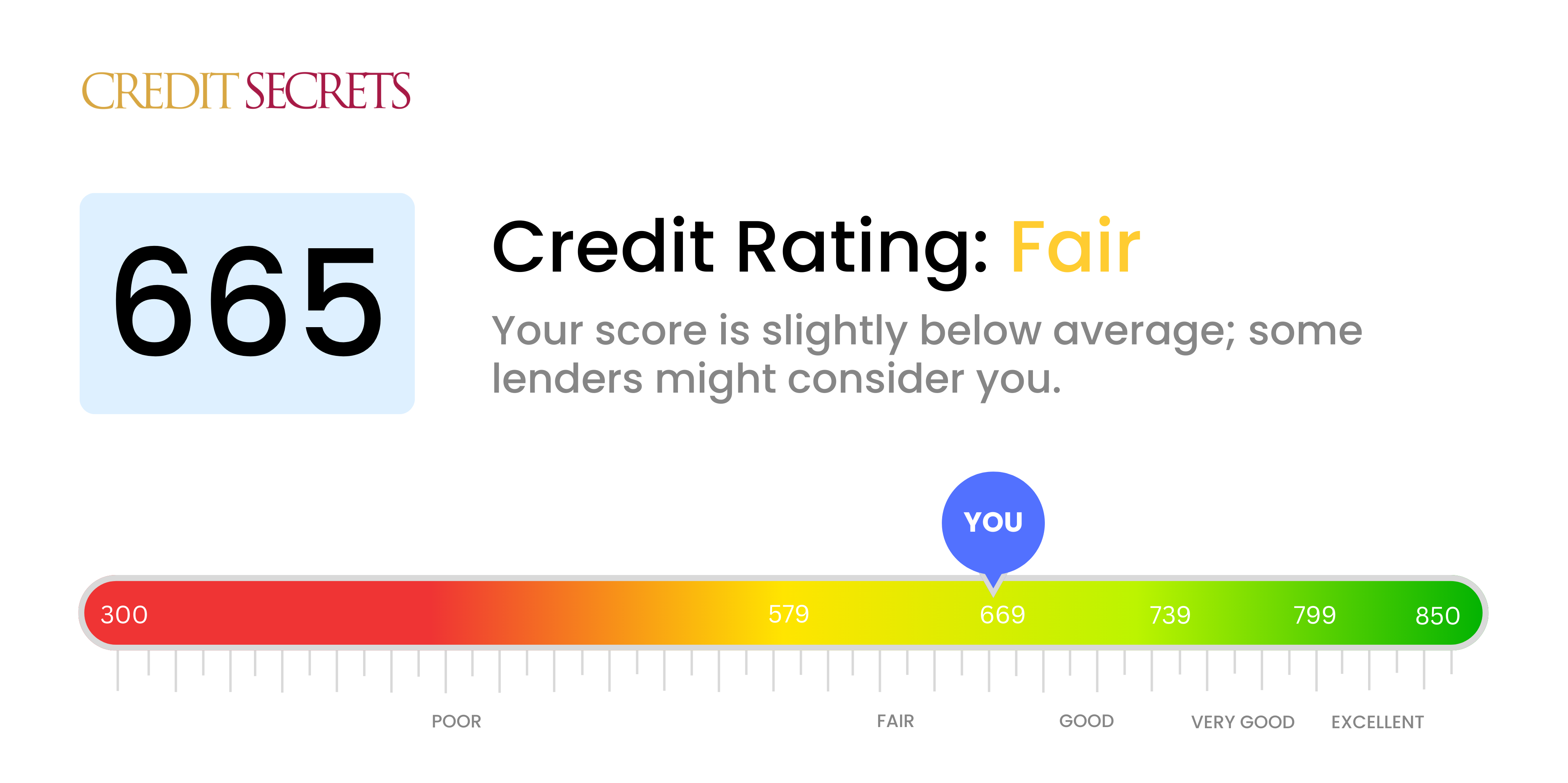

Can I Buy A House With A 665 Credit Score

So, you're dreaming of owning a home? Picture it: backyard barbecues, maybe a quirky pet, and finally ditching your landlord. You've even checked your credit score. It's a 665. Now the big question: Can you actually buy a house with that?

The Truth About Credit Scores

Let's be honest. Credit scores can feel like a secret code. Like some financial wizard is judging your life choices. But here's an "unpopular" opinion: they're not the be-all and end-all.

A 665 isn't terrible. It usually falls in the "fair" range. It's not amazing. But, hey, it's not rock bottom either!

Must Read

Think of it like this. It's a starting point. We can work with this!

Is a 665 Enough? Maybe!

The short answer? Maybe. It depends on a few things. Like, a lot of things. But don't despair just yet!

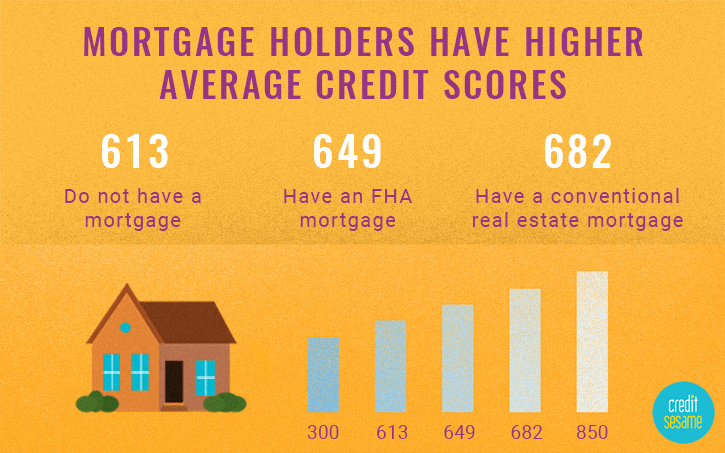

First, consider the loan type. FHA loans are often more forgiving. They can be a good option with a lower credit score.

USDA loans are great if you are ok to live in rural area. And the credit score minimum requirements are lower than other loans.

Then there's your down payment. A bigger down payment can make lenders happier. It shows you're serious and reduces their risk.

Things That Matter More Than You Think

Your debt-to-income ratio is HUGE. This is how much of your income goes towards debt. Lenders want to see you can actually afford the mortgage!

A stable job history is key. Lenders like predictability. Knowing you have consistent income makes them feel warm and fuzzy.

Also, your overall financial picture matters. Do you have savings? Are you good at managing money? These things tell a story.

Don't underestimate the power of a good lender. Some specialize in working with borrowers who have less-than-perfect credit.

The "Unpopular" Opinion: Banks Aren't Always Right

Here's where I might ruffle some feathers. Banks aren't always right! They're businesses. They have their own risk tolerance levels.

Just because one bank says no doesn't mean they all will. Keep shopping around. You might be surprised.

I've seen people get mortgages with similar credit scores. It takes work. It takes research. But it's possible!

Boosting Your Chances

Okay, so how do you increase your odds? Start by tackling any outstanding debt. Even small improvements can help.

Check your credit report for errors. Dispute anything that's incorrect. It's your right!

Avoid opening new credit accounts. This can actually lower your score in the short term. Focus on what you have.

Think Outside the Box

Consider a co-signer. Someone with good credit can vouch for you. This reduces the lender's risk.

Look into down payment assistance programs. Many exist! They can provide grants or loans to help with your down payment.

Explore alternative lending options. Credit unions or community banks might have more flexible requirements.

The Bottom Line

Can you buy a house with a 665 credit score? It's not guaranteed. But it's definitely not impossible.

It requires effort, research, and maybe a little bit of luck. But don't let that number define you.

Remember, a credit score is just a piece of the puzzle. So go out there. Find your dream home!

Don't Give Up!

Buying a home is a big deal. It's exciting and stressful. But don't let a less-than-perfect credit score stop you from pursuing your dream.

Do your homework. Be persistent. And never underestimate the power of a little optimism.

Who knows? You might be hanging those backyard barbecue lights sooner than you think!

Final Thoughts

So, what's the real takeaway? Credit scores are important. But they're not the only thing that matters.

Your financial health, your determination, and your ability to think outside the box can all play a role. A 665 is not a dead end!

Now, go get that house! You deserve it.