Can You Get Money Back On A Fha Loan

Let's face it, the idea of buying a home is a dream for many. It's about building a future, planting roots, and finally having a place to call your own. And for many first-time homebuyers or those with less-than-perfect credit, an FHA loan can be the key to unlocking that dream. They offer more lenient credit requirements and lower down payments, making homeownership accessible to a wider range of people. But what happens after you've secured that FHA loan? Is there a chance to get some of that money back? The answer is a bit nuanced, but exciting possibilities exist!

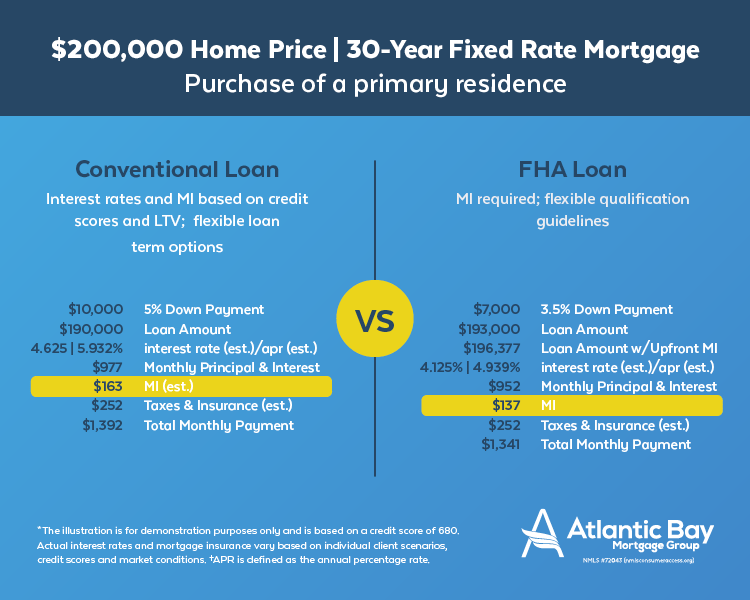

The main benefit of an FHA loan lies in its accessibility. Backed by the Federal Housing Administration, these loans are designed to help people who might not qualify for conventional mortgages. The purpose they serve is clear: to promote homeownership and stabilize communities. They allow individuals and families to build equity, create financial security, and contribute to the local economy. Imagine being able to finally afford that starter home, the one that allows you to begin building a life for your family – that's the power of an FHA loan.

Common examples of FHA loan usage include first-time homebuyers purchasing single-family homes, individuals refinancing existing mortgages to secure better interest rates, and families utilizing the FHA 203(k) loan to renovate and improve properties. Think of it as a tool to not just buy a house, but to improve a house, and by extension, your quality of life. But where does the "getting money back" part come in? There are a few scenarios.

Must Read

One avenue is through refinancing. As your credit score improves and interest rates fluctuate, you might be eligible to refinance your FHA loan into a lower-rate loan, either another FHA loan or even a conventional mortgage. This doesn't give you cash back upfront, but it does lower your monthly payments, effectively freeing up cash each month that you can use for other things. Over the life of the loan, this can add up to significant savings!

Another way, although less common, is through a cash-out refinance. This involves refinancing your existing mortgage for a larger amount than what you currently owe. The difference between the new loan amount and your old loan balance is then given to you in cash. However, beware of this option. While it might seem tempting, you're essentially adding debt to your mortgage, which means higher monthly payments and more interest paid over the long term. Only consider this if you have a very specific and financially sound plan for using the extra cash, such as home improvements that will significantly increase your property value.

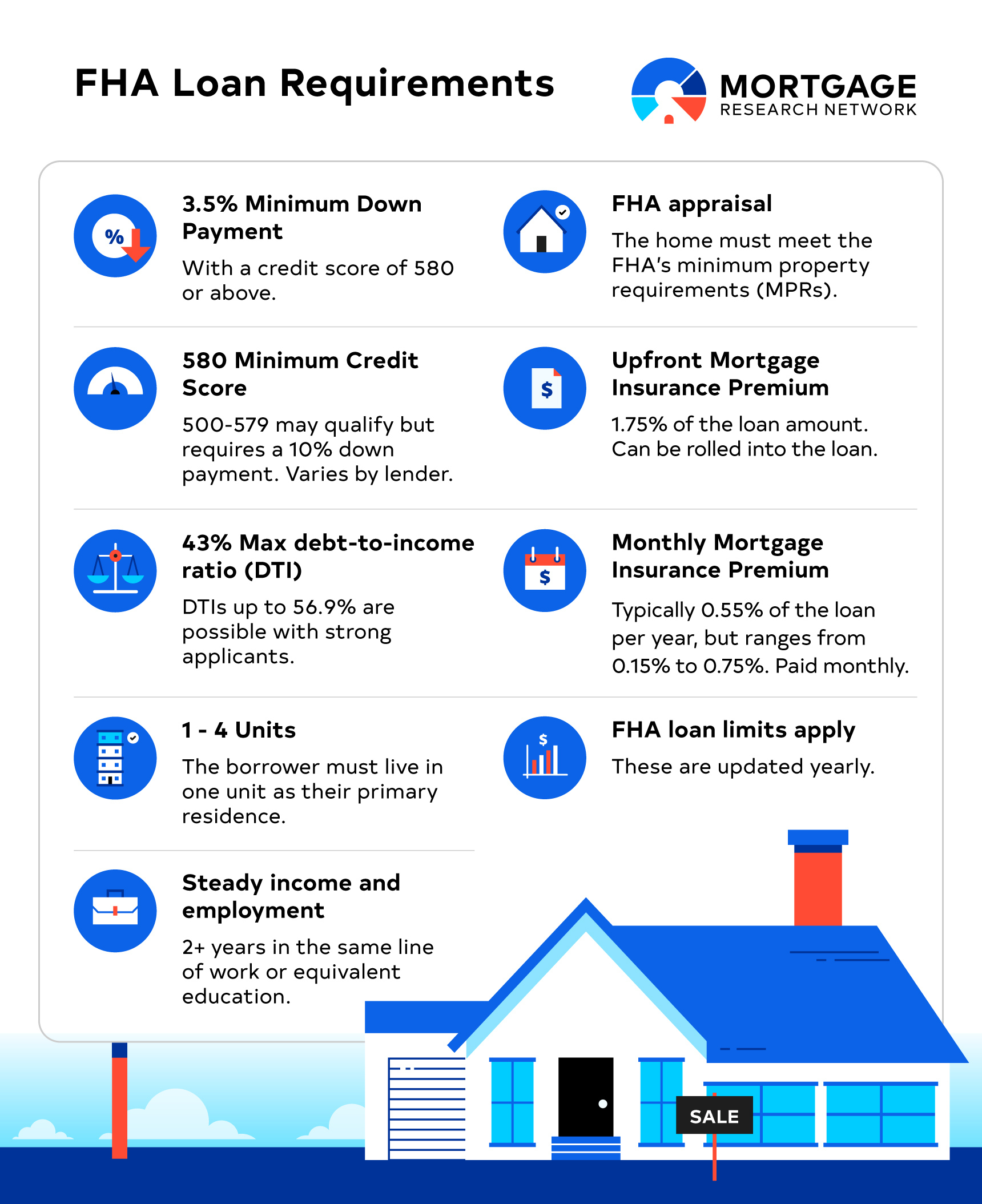

Finally, keep a close eye on your FHA mortgage insurance premium (MIP). This is an insurance payment you make as part of your FHA loan to protect the lender if you default. For loans originated after certain dates, this premium may be required for the life of the loan. However, depending on the loan terms and your loan-to-value ratio, there might be a point where you can request to have the MIP removed. Consult with your lender to understand your specific situation and explore your options.

To enjoy the benefits of an FHA loan more effectively, and potentially get some "money back" indirectly, focus on improving your credit score, staying current on your payments, and monitoring interest rate trends. Financial literacy is key! Understanding the terms of your loan and exploring your refinancing options can save you thousands of dollars over the life of your mortgage. So, while you might not get a literal check in the mail, strategically managing your FHA loan can certainly lead to significant financial gains.