Do Utility Bills Affect Your Credit Score

Ever wonder if keeping the lights on impacts more than just your wallet? We're talking about your credit score! Let's dive into the curious world of utility bills and credit.

The Credit Score Mystery

Credit scores. They’re like secret numbers that determine our financial fate. Want a car loan? A mortgage? Your credit score is a key player.

But what actually affects this magical number?

Must Read

The Usual Suspects

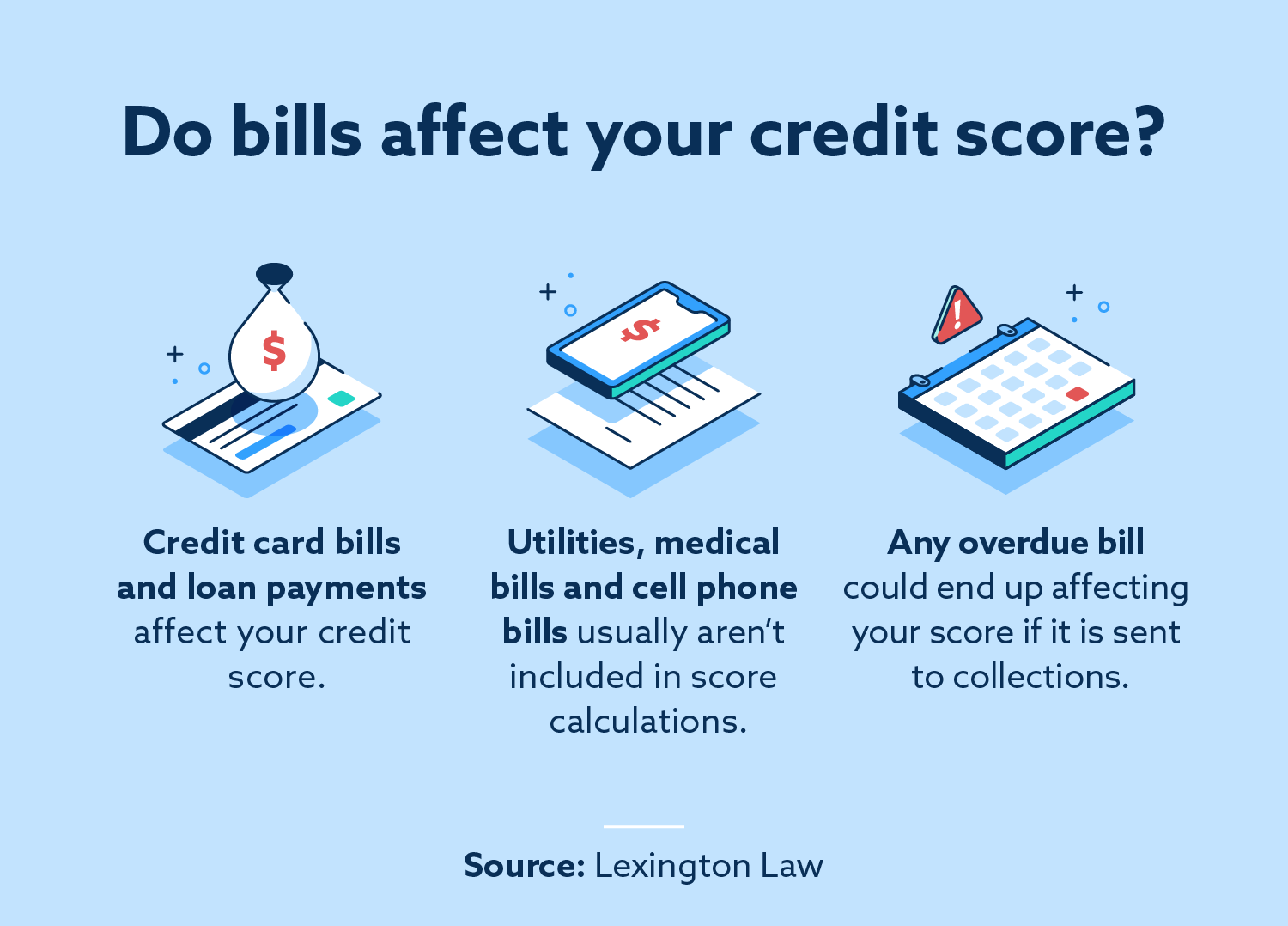

We know credit cards and loans play a big role. Paying those on time is like giving your credit score a high-five. Miss a payment? That’s a frownie face for your credit.

But what about those other bills? The ones that keep our homes comfy and connected?

Utility Bills: The Underdogs

Now, here’s where things get interesting. Think about your electricity, gas, water, and internet bills.

Do these everyday expenses influence your credit score? The answer might surprise you!

The Good News (Mostly)

Generally, paying your utility bills on time doesn't directly boost your credit score. Major credit bureaus, like Experian, Equifax, and TransUnion, typically don't track these payments.

Think of it like this: they’re not actively looking for you to be a responsible bill payer in that department.

The Bad News (Potentially)

However, there's a catch! Missed payments can come back to haunt you. Seriously late payments can end up in collections.

And guess what? Collection agencies do report to the credit bureaus. This is where your utilities can become a credit score villain.

When Utilities Attack Your Credit

So, how does a simple electricity bill turn into a credit score nightmare?

Let's paint a picture. Imagine you forget to pay your electricity bill for a couple of months. The utility company tries to contact you, but no luck.

Eventually, they send your unpaid bill to a collection agency. This is the point where things get serious.

The Collection Agency Cometh

Collection agencies are in the business of recovering debts. They'll likely contact you aggressively to get you to pay up.

And here's the kicker: they often report unpaid debts to the credit bureaus. This negative mark on your credit report can significantly lower your credit score.

A Credit Score Disaster

A collection account on your credit report is a big red flag to lenders. It suggests you have a history of not paying your bills on time.

This can make it harder to get approved for loans, credit cards, and even rent an apartment.

Building Good Credit Habits (Even with Utilities)

So, what can you do to protect your credit score from the utility bill monster? The answer is simple: pay your bills on time!

Here are a few tips to keep those utilities in check:

Budgeting is Your Best Friend

Create a budget that includes all your utility bills. This helps you track your expenses and ensure you have enough money to cover them.

There are tons of apps and tools that can help you with budgeting. Find one that works for you and stick with it!

Set Up Automatic Payments

Many utility companies offer automatic payment options. This is a great way to avoid late fees and ensure your bills are paid on time, every time.

Set it and forget it! Just make sure you have enough money in your account to cover the payments.

Communicate with Your Utility Company

If you're having trouble paying your bills, contact your utility company immediately. They may be able to offer payment plans or other assistance programs.

Ignoring the problem will only make it worse. Communication is key!

Check Your Credit Report Regularly

It's a good idea to check your credit report periodically for any errors or inaccuracies. You're entitled to a free credit report from each of the major credit bureaus every year.

Catching and correcting errors can help you maintain a healthy credit score.

Alternative Credit Data: A Glimmer of Hope?

There's a growing movement to include utility payments in credit scoring. This is where alternative credit data comes in.

Some companies are exploring ways to use utility payment history to help people with thin or no credit files build credit. This is especially helpful for those who are new to credit or have limited credit history.

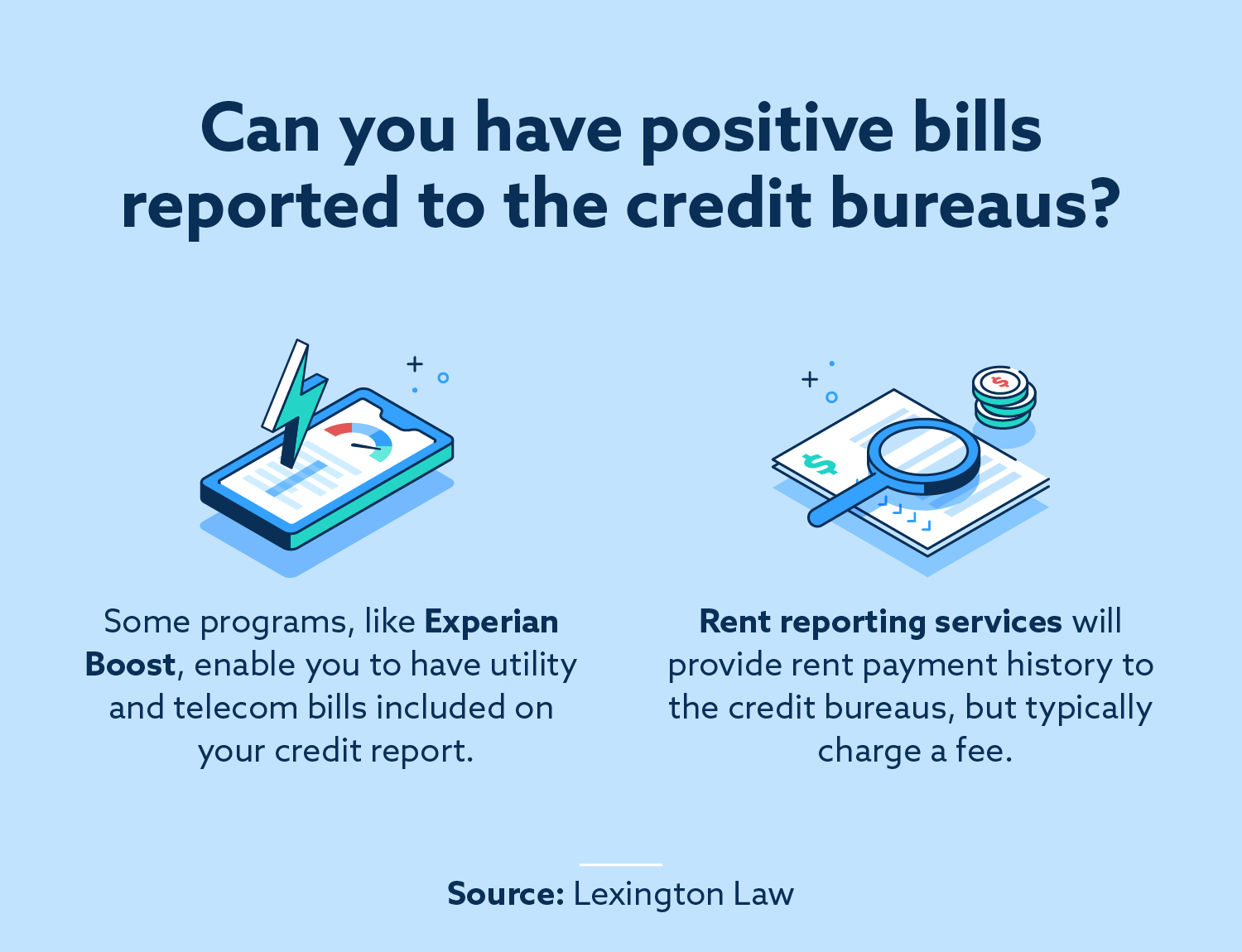

Experian Boost: A Step in the Right Direction

Experian Boost is one example of a program that allows you to add utility payments to your Experian credit report.

By linking your bank account to Experian Boost, you can get credit for on-time utility payments. This can potentially increase your credit score.

Rent Reporting Services

Similarly to Experian Boost, rent reporting services can help you get credit for on-time rent payments.

While rent isn't a utility, it's another recurring bill that can demonstrate your ability to manage your finances responsibly.

The Future of Credit Scoring

The way we assess creditworthiness is constantly evolving. Alternative credit data is becoming increasingly important.

In the future, utility payments may play a more significant role in credit scoring. This could help more people access credit and achieve their financial goals.

Stay Informed and Proactive

Keep an eye on the latest developments in credit scoring. Be proactive about managing your bills and building a positive credit history.

A little effort can go a long way in protecting your financial future.

The Bottom Line: Pay Your Bills!

So, do utility bills affect your credit score? The short answer is: indirectly, but potentially yes!

While paying them on time doesn't usually boost your score, failing to pay them can definitely hurt it.

Stay vigilant, budget wisely, and keep those bills paid to keep your credit score happy and healthy. And who knows, maybe one day paying your Netflix bill will help you buy a house!

Remember the Power of On-Time Payments

Don't underestimate the power of consistent, on-time payments. Whether it's your credit card, your rent, or your electricity bill, paying on time is the foundation of good credit.

It shows lenders that you're a responsible borrower and that you can be trusted to repay your debts.

Knowledge is Power

Understanding how your credit score works is essential for making informed financial decisions. The more you know, the better equipped you'll be to manage your credit and achieve your financial goals.

So, keep learning, stay informed, and take control of your credit future!