Do You Need Flood Insurance In A 500 Year Floodplain

Let's face it, nobody wants to think about flood insurance. It's right up there with root canals and tax audits on the list of fun things to contemplate. But, just like those other less-than-thrilling topics, understanding flood insurance can save you a lot of pain – and money – in the long run. We all love the peace of mind that comes from knowing our homes and belongings are protected, and that's precisely what flood insurance offers.

So, why do we need flood insurance anyway? Think of it as a safety net for your most valuable asset: your home. Your standard homeowner's insurance policy typically doesn't cover flood damage. Flooding can result from a variety of sources, including heavy rainfall, overflowing rivers or lakes, coastal storms, and even failed levees or dams. The damage can be devastating, leaving you with costly repairs and the emotional distress of losing personal belongings.

Flood insurance provides financial protection against these losses. It can cover the cost of repairing or replacing your home's structure, including walls, floors, and essential appliances. It can also cover your personal belongings, such as furniture, clothing, and electronics. In short, it helps you get back on your feet after a flood, without being completely financially crippled.

Must Read

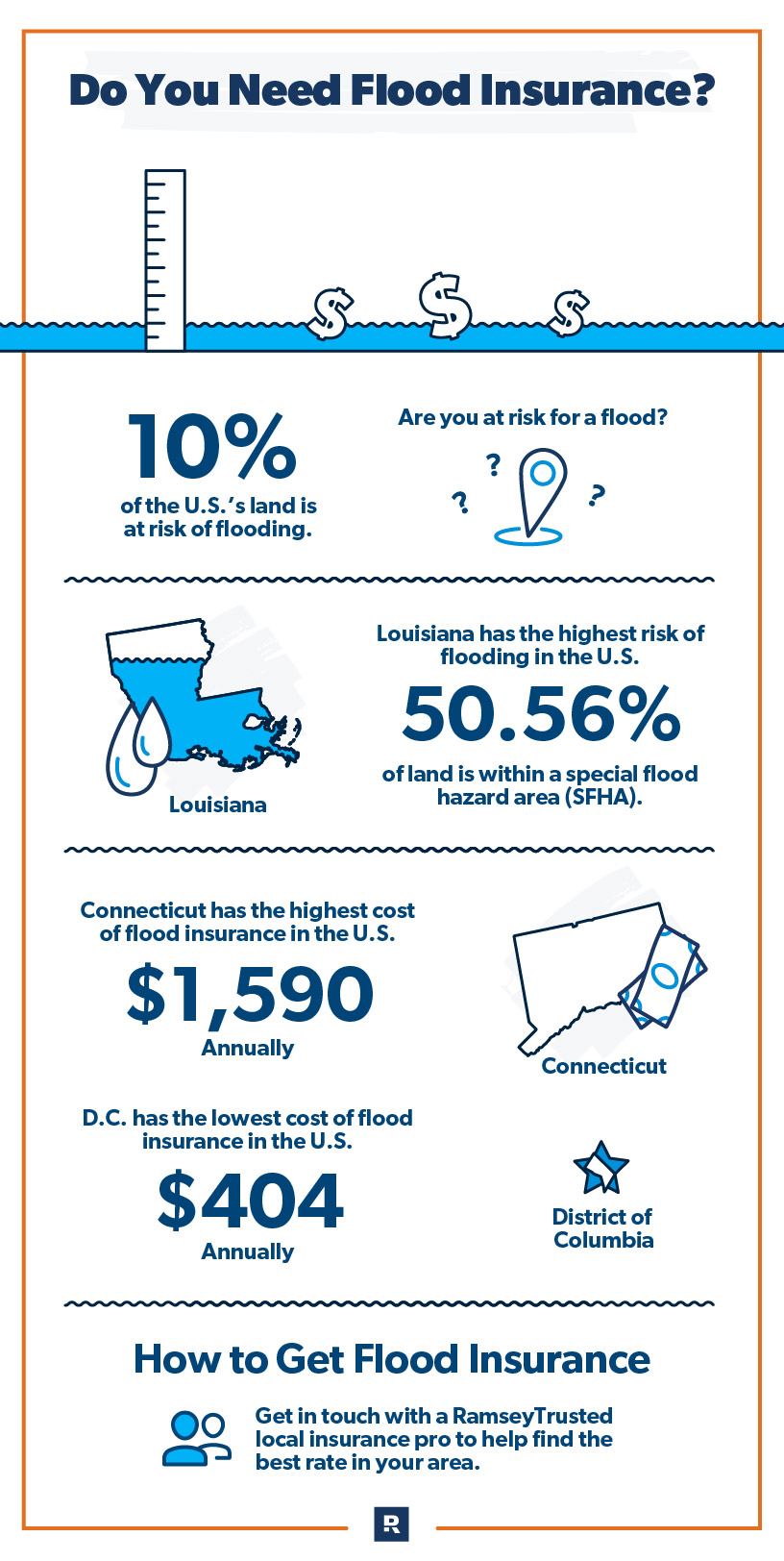

Now, let's get to the crux of the matter: do you need flood insurance if you live in a "500-year floodplain?" A 500-year floodplain is an area that has a 0.2% chance of flooding in any given year. While that might sound reassuringly low, it doesn't mean you're immune to flooding. Think of it like this: it's a probability, not a guarantee. A “100-year” or “500-year” flood can happen any year. Here's why it's still wise to consider flood insurance:

Firstly, flood risk maps are not perfect. They are based on historical data and modeling, which may not accurately predict future flooding events, especially in light of climate change. Weather patterns are changing, and extreme rainfall events are becoming more frequent and intense. What was once considered a "low-risk" area might be at greater risk than the map suggests.

Secondly, even shallow flooding can cause significant damage. Just a few inches of water can lead to thousands of dollars in damage to your home and belongings. Mold growth is a common consequence of flooding, and it can be expensive and difficult to remediate.

Thirdly, you might be required to have flood insurance even if you're in a 500-year floodplain. If you have a mortgage from a federally regulated lender, they might require you to carry flood insurance, regardless of your flood zone.

So, how can you make informed decisions about flood insurance? Here are some practical tips:

- Check your flood risk: Visit the FEMA Flood Map Service Center website (msc.fema.gov) to determine your property's flood zone.

- Get a flood insurance quote: Contact your insurance agent or the National Flood Insurance Program (NFIP) to get a quote.

- Understand your coverage options: Review your policy carefully to understand what is covered and what is not.

- Consider excess flood insurance: If you need more coverage than the NFIP offers, consider purchasing excess flood insurance from a private insurer.

- Take steps to reduce your flood risk: Implement measures such as elevating your utilities, installing flood vents, and improving drainage around your property.

Ultimately, the decision of whether or not to purchase flood insurance is a personal one. But consider the potential financial consequences of not having coverage. Weigh the cost of the premium against the potential cost of repairing or replacing your home and belongings after a flood. Even in a 500-year floodplain, the peace of mind that comes with knowing you're protected can be well worth the investment. Don't wait for the flood to come knocking – take proactive steps to protect your home and your future.