Does Paying A Power Bill Build Credit

Alright, settle in folks, grab a metaphorical coffee (or a real one, I won't judge), because we're about to tackle a question that's probably kept you up at night... maybe not, but hey, work with me here. Does paying your power bill actually build your credit? It’s a burning question, pun intended, that deserves some serious investigation. Prepare for a shocking (electricity pun, I'm on a roll!) truth.

So, imagine this: You diligently pay your electricity bill every month, on time, like the responsible adult you are. You're practically a saint of fiscal responsibility! You picture your credit score soaring to majestic, eagle-like heights. You dream of low interest rates and easy approvals for that yacht you've always wanted... okay, maybe a slightly less extravagant dream, like a new dishwasher. But the point is, you expect some credit karma points, right?

The brutal truth? Mostly... no. I know, devastating. Like finding out the Santa isn't real. Or that your cat actually hates the sweater you knit him. It stings. But don't throw your hands up in despair just yet. There's still a glimmer of hope, a tiny spark of electricity (I promise to stop... mostly) in this otherwise gloomy credit landscape.

Must Read

The Credit Bureau Breakdown: Who's Watching?

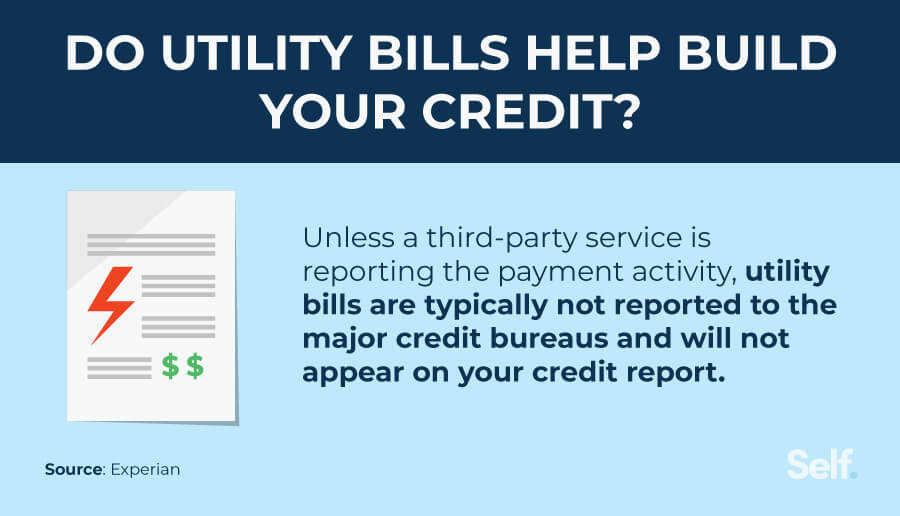

Here's the deal. Your credit score, that magical number that dictates your financial destiny, is primarily determined by three major credit bureaus: Experian, Equifax, and TransUnion. These guys are the gatekeepers to creditworthiness. They track your credit card usage, loan repayments, and other financial obligations. Now, here's the kicker: most utility companies don't regularly report your payment history to these credit bureaus.

Think of it like this: you're performing an awesome dance routine in your living room, but nobody's filming it. Sure, you feel good about yourself, but it's not going to get you on "Dancing with the Stars," you know? Unless, of course, you're secretly a viral sensation. Which, hey, maybe you are! But I digress.

So, why don't they report? Well, it's complicated. Setting up the infrastructure to report all those payments for all those customers is expensive and, frankly, a bit of a hassle. Plus, utility companies are more focused on keeping the lights on (or the gas flowing, or the water running) than boosting your credit score. They're busy with bigger fish to fry, like squirrels causing blackouts and explaining why your bill is higher in July when you were clearly on vacation.

The Exception to the Rule: When the Lights Shine Bright

Now, before you completely lose hope and start questioning the meaning of life, there's a loophole! A beautiful, credit-score-boosting loophole. Some utility companies do report to credit bureaus, especially if you're consistently late on payments. Think of it as a "naughty list" for your credit report. Ouch.

And here's another twist! There are also services, like Experian Boost, that allow you to voluntarily report your utility payments. Basically, you give them access to your bank account, they track your on-time payments, and then they report that positive information to Experian. It's like hiring your own personal credit score cheerleader. "Go you! You paid your electric bill! You're amazing!"

Experian Boost is like the underdog story of credit building. It's not a guaranteed slam dunk, but it can definitely help, especially if you have a limited credit history or are trying to rebuild your credit score.

What Can You Do? Power Up Your Credit Anyway!

Okay, so paying your power bill might not be the express lane to a perfect credit score. But fear not, intrepid credit builder! Here are some other ways to shine brighter than a freshly changed lightbulb:

- Credit Cards: Use them responsibly! Pay your balance on time and keep your credit utilization low (ideally below 30%). This is the bread and butter of credit building.

- Secured Credit Cards: If you have bad credit or no credit, a secured credit card is a great way to start. You put down a deposit, which acts as your credit limit, and then you use the card like a regular credit card.

- Credit-Builder Loans: These loans are designed to help you build credit. You make fixed payments over a set period, and your payment history is reported to the credit bureaus.

- Become an Authorized User: Ask a friend or family member with good credit to add you as an authorized user on their credit card. Their positive payment history will be reflected on your credit report (but beware, their negative history will too!).

The bottom line? Paying your power bill is important, obviously. Nobody wants to live in the dark ages (literally). But if you're looking to boost your credit score, focus on those key areas: credit cards, loans, and those clever credit-building services. And remember, be responsible, pay on time, and don't let your credit score become a horror story!

Now if you'll excuse me, I need to go pay my own electricity bill. Wouldn't want to be a hypocrite, would I?