Due Date Vs Statement Date

Picture this: you’re at your favourite café, steam curling from your mug, trying to explain to a friend why their credit card statement just sent them into an existential spiral. They’re staring wide-eyed at a piece of paper, muttering about dates and numbers like they’ve just decoded an alien message. “But… but what’s the difference between the due date and the statement date?” they wail, as if I’ve just asked them to solve the unified field theory.

Ah, my friend. Welcome to the thrilling, often confusing, world of personal finance jargon! It’s less alien message, more like a secret handshake that no one bothered to teach you. But fear not, for today we unravel this mystery, with a side of humour and perhaps a slightly exaggerated anecdote or two.

The Statement Date: When the Whistle Blows!

Let’s start with the statement date. Think of it as the official finish line for a specific billing period. Imagine you’re at a ridiculously competitive pie-eating contest (don’t ask, just imagine). The statement date is when the referee blows the whistle and shouts, “Pencils down! Or rather, forks down!”

Must Read

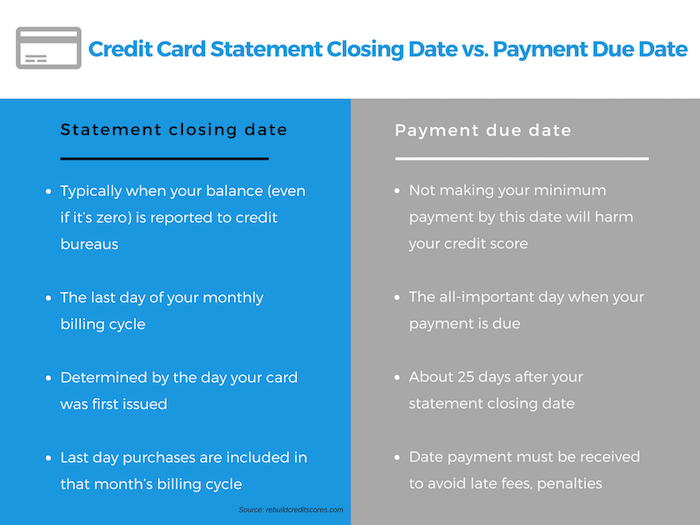

This date marks the end of a cycle, usually lasting about 30 days. On this particular day, your credit card company (or whoever you owe money to) takes a snapshot. They look at everything you’ve spent, paid, or received in credits since your last statement date, and they say, “Boom! This is your bill for this period!”

It’s the day your financial snapshot is taken, a frozen moment in time. So, if your statement date is the 15th of the month, anything you bought on the 16th won’t appear on this bill. It’s off to the next billing cycle, like a sneaky chocolate bar you hid from your kids – out of sight, out of mind (for now).

Here’s a fun fact, or at least a surprising one: your statement date is often the same day every single month. Predictable, right? And yet, how many of us actually remember it? It’s like forgetting your own phone number – you use it all the time, but ask you to recite it, and suddenly it’s gone!

The Due Date: The Ultimate Deadline!

Now, onto the due date. This is where things get a little more… urgent. If the statement date is when they tally up your pie consumption, the due date is when they demand payment for said pie. And if you don’t pay up, well, let’s just say there might be consequences.

The due date is simply the deadline for you to pay at least the minimum amount due on that statement. Miss this date, and prepare for the financial equivalent of a slap on the wrist – which often comes in the form of a late fee and potentially a ding to your credit score. Ouch! Nobody wants a credit score that looks like it lost a fight with a badger.

Here’s the surprisingly generous bit: the due date is typically set about 20 to 25 days after your statement date. That’s a whole grace period! Think of it as your credit card company giving you a nice, comfortable cushion of time to gather your funds, count your pennies, and maybe even find a few forgotten crumpled bills in your old jeans.

It’s like your professor giving you three weeks after the assignment is handed out to actually turn it in. Except instead of an "F" for being late, you get a "F" for "fee" and "frustration."

The Crucial Difference & Why It Matters More Than You Think

So, to sum it up: the statement date tells you what you owe, and the due date tells you when you need to pay it. Simple, right? Yet, this is where so many intelligent, well-meaning people trip up.

Mixing these two up can lead to paying late, incurring fees, and stressing yourself out unnecessarily. Imagine thinking your bill is due on the 15th (your statement date) only to realize you had until the 10th of the next month (your actual due date). Or, worse, thinking it’s due on the 10th of the next month, when it was actually the 15th of this month! Confusion is the enemy of your wallet.

The 20-25 day grace period between these two dates is your golden ticket. It’s not just a buffer; it’s a strategic window to pay your bill in full and avoid interest charges. That’s right! If you pay your entire statement balance before the due date, you typically pay zero interest on those purchases. It’s like a magical free loan!

Be a Financial Superhero, Not a Financial Zero!

Understanding these dates turns you from a bewildered café patron into a financial ninja. Here are your secret weapons:

- Automate your payments: Set up an automatic payment for at least the minimum amount by the due date. Better yet, set it for the full statement balance. Future you will send present you a thank-you note (probably with a cake).

- Know your dates: Seriously, write them down. Put them in your calendar. Tattoo them on your forehead if you must (but maybe just use a calendar).

- Pay the full statement balance: If you can, always pay the entire statement balance by the due date. This is how you escape the clutches of interest and truly leverage the benefits of credit. If you only pay the minimum, you’ll be paying interest on the remaining balance, and those magical pies start to get very, very expensive.

So, the next time you see that credit card statement, don't just stare at it like it's a cryptic treasure map. Understand the two most important dates on it. One tells you the total loot you've accumulated, the other tells you when to hand over your gold. Master them, and you’ll find yourself much wealthier in peace of mind, and probably in actual money too.

Now, about that second cup of coffee…