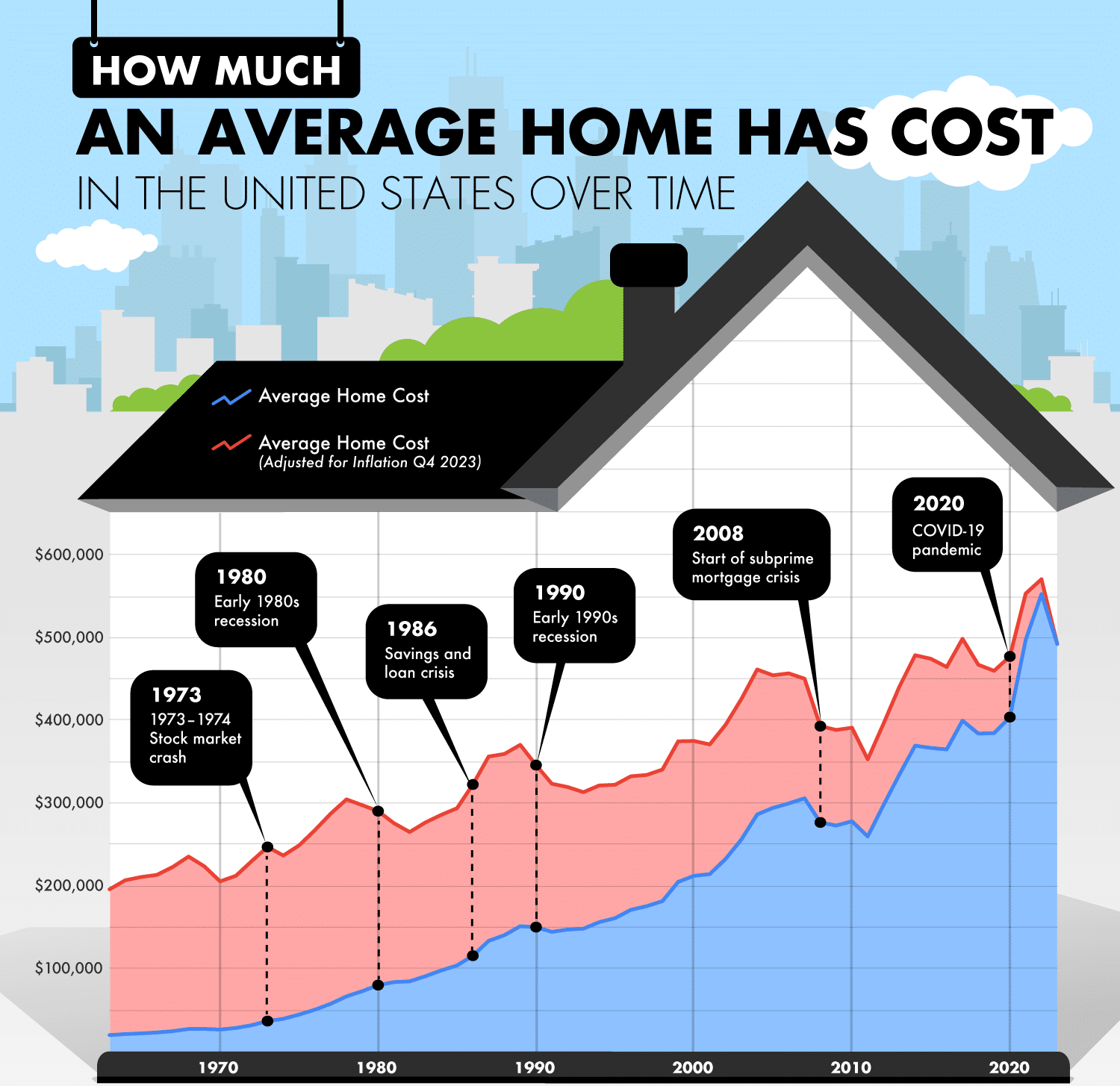

How Much Is The Average House Cost

So, how much does the average house REALLY cost? Let's dive in. Buckle up, buttercup!

The Million-Dollar Question (Literally?)

Finding an exact "average" house cost is trickier than assembling IKEA furniture. Numbers dance around like mischievous gremlins. It feels like everyone has a different number.

One minute you're reading about a national average. Next, it's broken down by state, county, and then...your specific street! Data overload, anyone?

Must Read

The "Official" Numbers Game

Websites throw around figures like confetti at a parade. They cite median sales prices, average listing prices, and even whispers Zestimates. Who even trusts Zestimates?

It’s all a blur of commas and dollar signs. You start questioning reality. Are these real houses? Or some sort of digital unicorn dwellings?

The thing is, "average" is a slippery fish. It depends on so many factors. Location, size, condition...the list goes on forever.

My (Unpopular) Opinion: It's All Relative

Here's my hot take: the "average" house cost is irrelevant. Yes, I said it! Don't @ me.

What really matters is what a house costs you. What can you afford? That's the golden question.

Comparing yourself to national averages is a recipe for stress. Focus on your own financial reality. Your sanity will thank you.

Decoding the Housing Market Lingo

Navigating the housing market is like learning a new language. There are so many terms to understand.

Think "mortgage," "escrow," "appraisal"... It's enough to make your head spin!

Let's break down some common terms to make things a little less scary.

Mortgage Mayhem: Your Loan Options

A mortgage is basically a loan you take out to buy a house. It's a big commitment.

There are different types of mortgages. Fixed-rate, adjustable-rate...the possibilities are endless.

Do your research. Talk to a lender. Find the best option for your situation. And for Pete's sake, read the fine print!

Down Payment Drama: How Much Do You Need?

The down payment is the amount of money you pay upfront. It's usually a percentage of the purchase price.

Traditionally, 20% was the standard. But these days, lower down payment options exist. It can be as low as 3%.

Lower down payments mean higher monthly payments. Weigh the pros and cons carefully.

Closing Costs Chaos: The Hidden Fees

Closing costs are fees associated with finalizing the home purchase. Think of them as sneaky extras.

They can include appraisal fees, title insurance, and recording fees. Budget for these expenses. They can add up quickly.

Negotiate if you can! Every dollar saved is a dollar earned (or, you know, not spent).

Location, Location, Location: The Ultimate Factor

Where you want to live plays a HUGE role in house prices. It's the age-old real estate mantra.

A shack in Malibu? Astronomical. A mansion in rural Nebraska? Surprisingly affordable.

Consider your priorities. What's important to you in a location? Proximity to work? Good schools? Access to amenities?

City Slickers vs. Suburban Serenity

City living usually comes with a hefty price tag. Space is limited, demand is high.

Suburbs offer more space for your money. But you might sacrifice convenience and commute time.

Think about your lifestyle. Which environment suits you best? Are you a city person or a country person?

The Commute Conundrum: Time is Money

Don't underestimate the impact of your commute. It can affect your quality of life.

Long commutes can lead to stress and wasted time. Factor in gas prices, car maintenance, and tolls.

Sometimes, paying a bit more for a shorter commute is worth it. Your sanity will thank you, again!

House Hunting Hacks: Finding Your Dream Home (Without Breaking the Bank)

So, how do you find your dream home without emptying your bank account? Here are a few tips.

Be realistic. Know your budget. Don't fall in love with houses you can't afford. (Easier said than done, I know!)

Get pre-approved for a mortgage. This shows sellers you're a serious buyer. It also helps you understand your borrowing power.

Shop Around: Compare Mortgage Rates

Don't settle for the first mortgage rate you get. Shop around and compare offers. Even a small difference can save you thousands over the life of the loan.

Credit unions, banks, and online lenders all offer different rates. Do your homework and find the best deal.

Consider working with a mortgage broker. They can help you find the best rates from multiple lenders.

Negotiate Like a Boss: Don't Be Afraid to Ask

Don't be afraid to negotiate on the price of the house. It's part of the game.

Point out any flaws or repairs that need to be made. Use these as leverage to lower the price.

Be prepared to walk away if the seller isn't willing to negotiate. There are other houses out there!

Consider a Fixer-Upper: Unleash Your Inner DIY-er

A fixer-upper can be a great way to save money. But proceed with caution. (Unless you actually know how to fix things.)

Get a thorough inspection before you buy. Factor in the cost of repairs and renovations. Make sure you have the skills (or the budget to hire someone) to complete the work.

DIY projects can be rewarding. But they can also be stressful and time-consuming. Be honest with yourself about your abilities.

The Bottom Line: It's All About Perspective

The "average" house cost is a moving target. Don't get too caught up in the numbers.

Focus on your own financial situation. What can you realistically afford? What are your priorities?

Buying a house is a big decision. Take your time, do your research, and don't be afraid to ask for help.

And remember, home is where the heart is. It's not just about the price tag. The best investment is in a place where you can build memories.

Good luck with your house hunting adventures! May the odds be ever in your favor.

And if you see me out there, knee-deep in mortgage paperwork, please bring coffee!