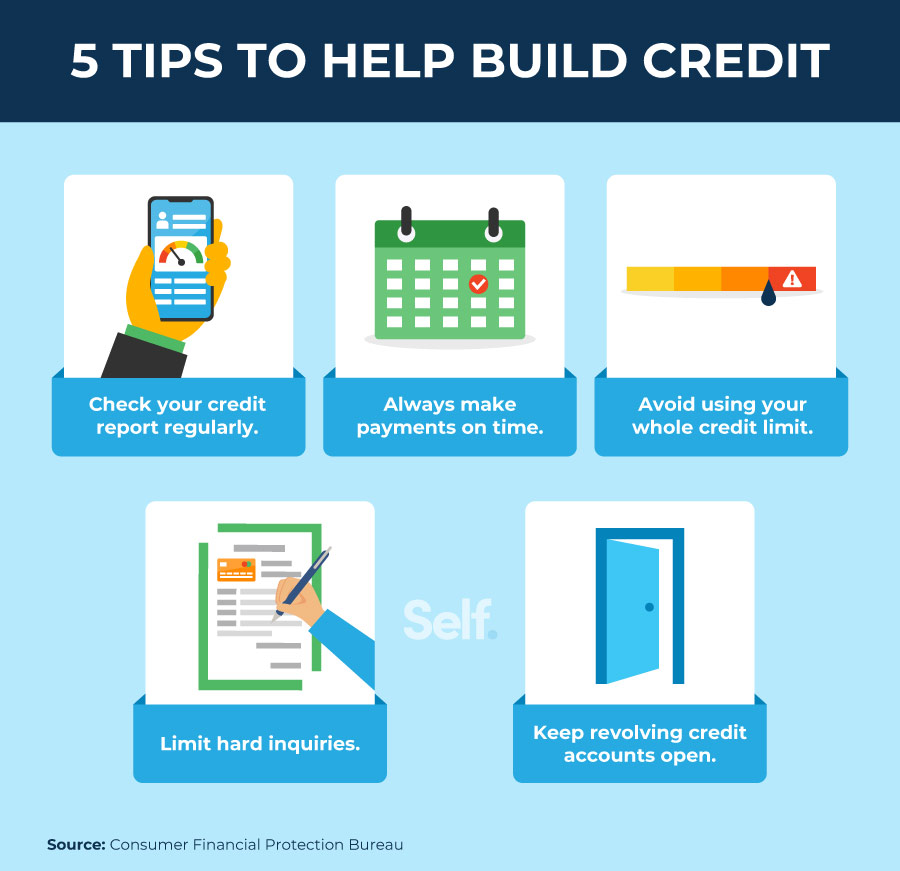

How To Add Bills To Credit Report

Alright, let's talk about credit scores. They're often seen as this mysterious, all-powerful number that dictates whether you get that dream apartment or a loan for a new car. It feels a bit like trying to appease a very specific, invisible dragon, doesn't it?

You’re diligently paying your credit card bills, maybe you’ve got a car loan humming along, and you’re thinking, “Surely, all these other responsible things I do count for something, right?” Well, friend, you're not wrong! What if I told you that some of those everyday payments you make – the ones that quietly disappear from your bank account each month – could actually be working hard to beef up your credit report?

The Unsung Heroes of Your Wallet

Imagine your credit report as a bustling city. You've got your skyscrapers (mortgages), your slick office buildings (credit cards), and maybe a nice townhouse (car loans). But what about all the other essential parts of the city? The buses, the streetlights, the park benches? Those are your rent, your utility bills, your internet subscription. They keep your life running smoothly, but for the longest time, they’ve been the unsung heroes, doing their job without getting a single credit-score high-five.

Must Read

That monthly rent payment that feels like it vanishes faster than a chocolate bar at a kids' birthday party? Or that internet bill that keeps you connected to your cat videos and late-night shopping sprees? They’re proof that you're reliable, responsible, and perfectly capable of managing your money. And now, thanks to some savvy financial folks, these payments can actually get the recognition they deserve.

Why Bother? Because Every Point Counts!

You know how in video games, even a small power-up can turn the tide of battle? Adding your rent and utility payments to your credit report is kind of like giving your credit score a mini-superpower. It's especially useful for people who are just starting out, or those who haven't had a lot of traditional credit history. Think of it as giving your credit profile a much-needed workout without breaking a sweat (or taking on more debt).

It can potentially help you:

- Boost your score, making you look more attractive to lenders.

- Diversify your credit mix, showing you can handle different types of payments.

- Prove your financial reliability, even if you’re not swimming in credit cards.

So, How Do We Get These Invisible Bills on the Record?

This isn't like calling up the credit bureaus and saying, "Hey, remember that time I paid my water bill on time? Add that!" Nope. It's a bit more nuanced than that. You can't just wave a magic wand (though that would be cool).

Step 1: Identify Your Credit Sidekicks

These are the regular, recurring payments that aren't already on your credit report. The usual suspects include:

- Rent: The big one for many.

- Utilities: Electricity, gas, water, sewage.

- Telecom: Internet, cell phone bills.

- Sometimes even streaming services, but those are less common for reporting services.

Think about the bills that hit your bank account like clockwork, every single month. Those are your potential credit heroes.

Step 2: Enlist a Reporting Service

Since you can't report these yourself, you need a middleman. Think of them as the special agents who translate your everyday payments into credit-speak. There are several services out there, and they generally fall into a couple of categories:

A. Direct Reporting Services: These are companies specifically designed to report your rent or utility payments to one or more of the major credit bureaus (Experian, TransUnion, Equifax). Examples include RentReporters, LevelCredit, and some others.

How they work: You usually sign up, link your bank account, and they scour your transaction history (with your permission, of course) to identify those regular rent or utility payments. Once they spot them, they then report that positive payment history to the credit bureaus. It's like having a financial detective on your side!

B. Credit Bureau Specific Programs: Some of the credit bureaus themselves have programs to help. Experian has Experian Boost, for example, which allows you to connect your bank account and potentially get credit for utility and telecom payments. It's pretty neat because it's free and can give your Experian score an immediate lift.

Step 3: What to Expect and Keep in Mind

Once you’ve signed up with a service, it’s not always instant magic. It takes a little time for the information to be processed and appear on your report. Also, remember:

- It’s not a universal fix. While some services report to all three bureaus, others might only report to one or two. So, check which bureaus they work with.

- Fees might apply. Many direct reporting services charge a monthly or annual fee for their service. Experian Boost is a shining exception, as it's free.

- Paying on time is paramount. If you’re late on a payment that's being reported, it could actually hurt your score. So, make sure you're consistent. This isn't a "get out of jail free" card for late payments; it's a "look how responsible I am" card!

- Results vary. Not everyone will see a massive jump, but any positive information added to your credit report is generally a good thing.

The Takeaway: Empower Your Everyday Spending!

Your credit score doesn't have to be a dark art. By proactively finding ways to add your regular, on-time payments for things like rent and utilities, you're taking control and turning those previously invisible acts of financial responsibility into powerful data points. It’s like finally giving those background characters in your financial movie the spotlight they deserve.

So, go forth! Explore your options, find a service that works for you, and start letting those everyday bills do some heavy lifting for your financial future. Your credit score – and your peace of mind – might just thank you for it!