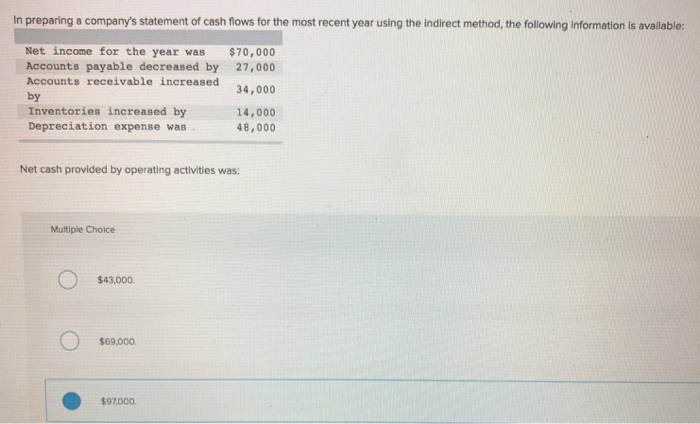

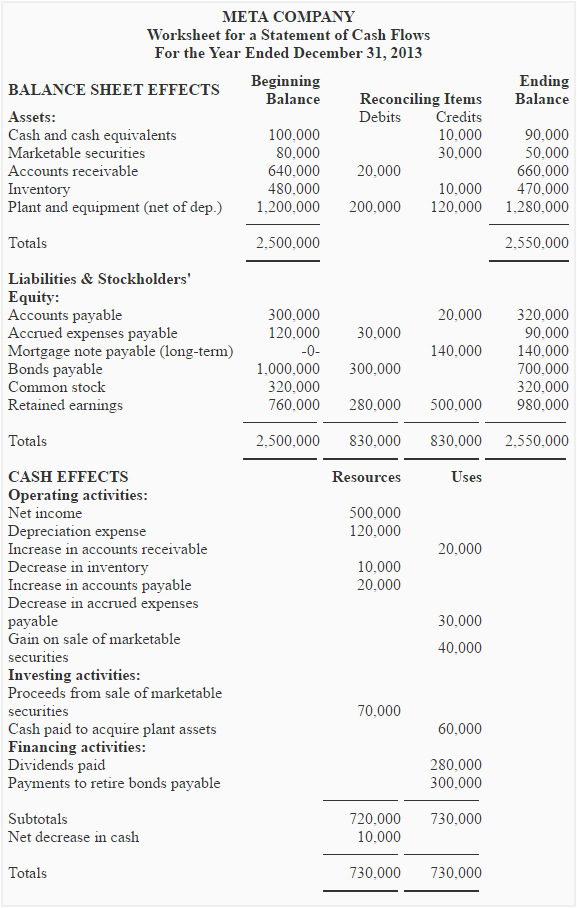

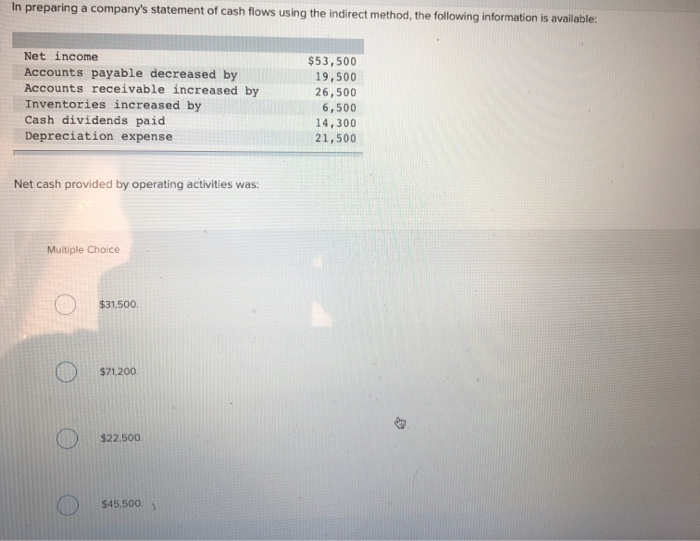

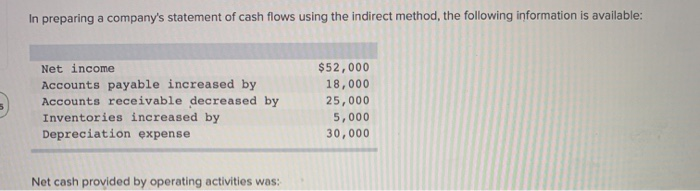

In Preparing A Company's Statement Of Cash Flows

Hey there, fellow finance fanatic! So, you're diving into the wonderful, sometimes-slightly-terrifying world of the Statement of Cash Flows, huh? Don't worry, it's not as scary as it sounds (promise!). Think of it as your company's financial diary, but instead of juicy gossip, it tracks where the cash comes from and where it goes. Exciting, right? Okay, maybe not "gossip" exciting, but still important!

Basically, the Statement of Cash Flows answers the big question: Where did all the money go? (And, more importantly, where did it come from?). It's super crucial for understanding a company's financial health. I mean, a company can look profitable on paper, but if it's bleeding cash, Houston, we have a problem!

First Things First: The Three Amigos (Activities, That Is!)

The Statement of Cash Flows is divided into three main sections, like a perfectly balanced financial trifecta. Each section represents a different type of activity.

Must Read

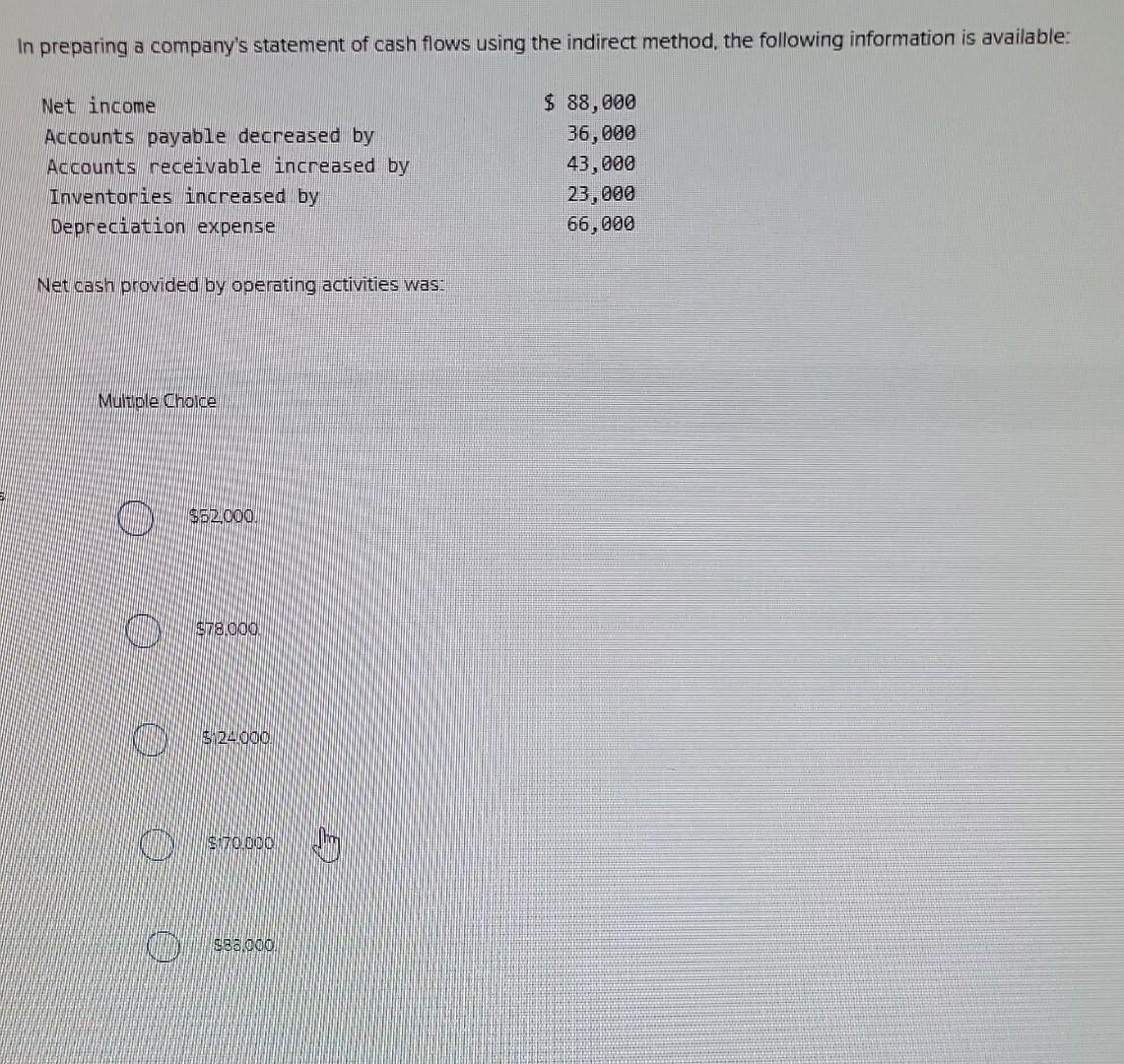

Operating Activities: This is where the real action is. Think of it as the heart of your business. It shows the cash generated (or, yikes, used!) from your day-to-day business operations. Selling stuff, paying employees, buying inventory – you know, the everyday grind. Figuring this out usually involves taking your net income from the income statement (that other fun document!) and adjusting it. Adjusting it, you say? Yep! Because net income includes non-cash items like depreciation. We need to eliminate those, since we only care about actual cash money in this game!

Investing Activities: This section deals with the buying and selling of long-term assets. Think of it as playing Monopoly...but with real money (and hopefully less arguing). Buying property, plant, and equipment (PP&E), purchasing securities, or lending money are all part of this game. Did you just invest in that shiny new robot for the factory floor? Congrats! That's an investing activity. Did you sell off some old equipment? Good job! That's investing, too!

Financing Activities: This section is all about how the company is funded. Borrowing money (hello, loans!), issuing stock, repaying debt, and paying dividends all fall into this category. Did you just take out a loan to expand your business? That's financing. Did you give investors a nice little dividend check? Yup, financing! It's basically how you're juggling your debts and equity, and trust me, juggling is exactly how it feels sometimes.

Direct vs. Indirect: Choose Your Own Adventure!

Now, for the Operating Activities section, you have a choice: the direct method or the indirect method. It's like choosing between vanilla and chocolate ice cream (both good, but different!).

The direct method shows the actual cash inflows and outflows. Basically, you list out all the cash received from customers, cash paid to suppliers, etc. It's pretty straightforward (hence the name!), but it can be a bit more work to gather all the data.

The indirect method, on the other hand, starts with net income and adjusts it for non-cash items and changes in working capital (accounts receivable, accounts payable, inventory, etc.). This method is more commonly used because the data is easier to get from the income statement and balance sheet. Many accountants prefer this.

So, which one should you choose? Well, the Financial Accounting Standards Board (FASB), those wise folks who set the accounting rules, prefers the direct method, but allows companies to use the indirect method. So, it's really up to you (or, more likely, your company's accounting policy). You should always disclose which method you use, of course. Transparency is key!

Putting It All Together: The Big Finale

Once you've figured out the cash flows from each activity, you add them all up to get the net increase (or decrease!) in cash for the period. Then, you add that to the beginning cash balance to get the ending cash balance. Voilà! You have your Statement of Cash Flows! (Okay, maybe there are a few more details, but that's the gist of it!).

Remember, this statement is incredibly important. It helps investors, creditors, and management understand a company's liquidity, solvency, and financial flexibility. It's like giving them a sneak peek into the company's bank account (but, you know, in a professional and ethical way!).

So, go forth and conquer the Statement of Cash Flows! You got this! And remember, when in doubt, consult a professional accountant (or, you know, just Google it...we've all been there!).