Minimum Requirements For Buying A House

Okay, let's talk about something seriously exciting: buying a house! It might seem like a huge, daunting thing, full of paperwork and complicated terms. But honestly, it's totally achievable, and it's the first step toward creating your very own personal haven. Think cozy movie nights, backyard barbecues, and painting the walls exactly the shade of avocado green you've always dreamed of! (Okay, maybe not avocado green, but you get the idea.)

So, what's the minimum you need to jump into the homeownership game? Let's break it down, shall we?

Credit Score: Your Financial Superhero (Or Sidekick!)

First up: your credit score. Think of it as your financial reputation. Lenders use it to figure out how likely you are to pay back your mortgage. A higher score means you're a reliable borrower, and that unlocks better interest rates. We're talking saving potentially thousands of dollars over the life of your loan!

Must Read

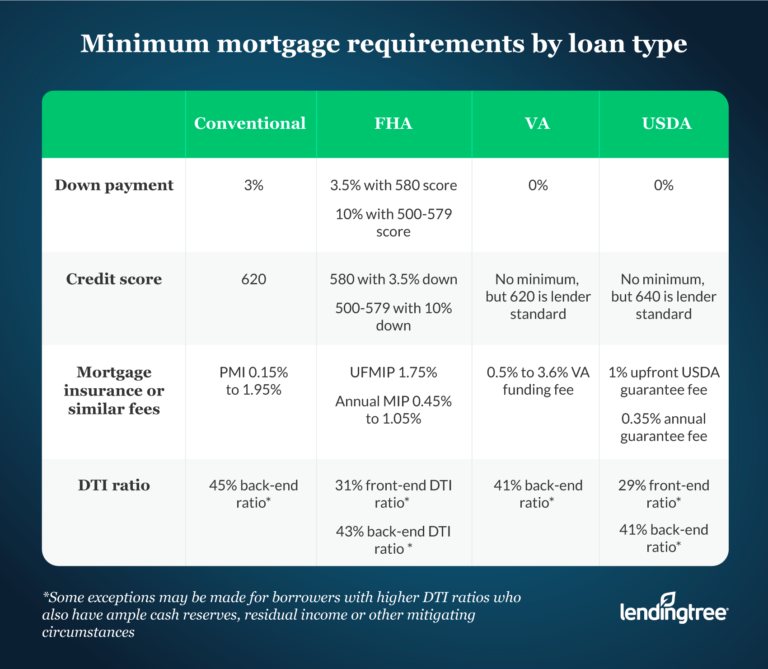

What's a good score? Generally, lenders like to see scores above 620. But hey, don't panic if you're not there yet! There are tons of ways to boost your score. Pay your bills on time (seriously, set reminders!), keep your credit card balances low, and check your credit report regularly for any errors. You got this!

Down Payment: Not as Scary as It Sounds

Next, we've got the down payment. This is the chunk of money you pay upfront when you buy the house. The traditional rule of thumb was 20%, which, let's be honest, can feel like climbing Mount Everest in flip-flops. But good news! Many loan programs now allow for much lower down payments, sometimes as low as 3% or even 0% for certain qualified buyers (like veterans – thank you for your service!).

Don't assume you need a massive pile of cash! Explore different loan options, like FHA loans, USDA loans, and VA loans. Each has its own eligibility requirements, so do your research and find the one that fits you best.

Debt-to-Income Ratio (DTI): The Balancing Act

Here's a fun one: Debt-to-Income Ratio (DTI). Basically, it's the percentage of your gross monthly income that goes towards paying off debts (like credit cards, student loans, and car payments). Lenders use this to see how much you can realistically afford each month. They want to make sure you're not stretched too thin!

A DTI of 43% or less is generally considered good. So, if you're carrying a lot of debt, now's the time to start strategizing! Consider paying down high-interest debts or exploring ways to increase your income. Every little bit helps!

Stable Income: Showing You're Ready to Commit

Lenders want to see that you have a stable and consistent income. This doesn't necessarily mean you need to have been at the same job for 20 years (though that certainly wouldn't hurt!). They just want to be reasonably sure that you'll be able to make your mortgage payments. Provide pay stubs, tax returns, and any other documentation that proves you have a reliable income stream.

Freelancers and self-employed individuals, don't despair! You'll just need to provide a bit more documentation to demonstrate your income stability, such as profit and loss statements. It's totally doable!

Pre-Approval: Your Secret Weapon

Before you even start house hunting, get pre-approved for a mortgage. This means a lender has reviewed your financial information and determined how much they're willing to lend you. A pre-approval letter shows sellers that you're a serious buyer, and it gives you a huge advantage in a competitive market. Plus, it helps you narrow your search to houses you can actually afford. Win-win!

The "Soft Skills": Don't Underestimate Them!

Beyond the numbers, there are some important "soft skills" you'll need. Being organized will help you keep track of all the paperwork involved. Having patience is crucial because the home-buying process can sometimes be slow and frustrating. And finally, being willing to learn is essential, as there's a lot to know about real estate. But hey, that's why you're reading this, right?

So, there you have it! The minimum requirements for buying a house. It might seem like a lot, but remember, you don't have to do it all at once. Take it one step at a time, and celebrate each milestone along the way. Buying a house is a big achievement, and it's something to be proud of. Imagine the possibilities! A space to truly call your own, to decorate however you like, and to create lasting memories with loved ones. It's an investment in your future, and it's a chance to build the life you've always dreamed of.

Ready to learn more and take the next step? Start researching local lenders, exploring different loan programs, and working on improving your credit score. The world of homeownership awaits! Go get 'em!