Personal Loan With Land As Collateral Bad Credit

Okay, let's talk about something that might seem a little daunting: personal loans when you've got less-than-stellar credit and you're thinking about using land as collateral. Sounds… intense, right? But honestly, it's not as scary as binge-watching a horror movie marathon alone. We're going to break it down, keep it light, and hopefully, leave you feeling a little more informed and a lot less stressed. Think of this as financial self-care, but with information instead of avocado face masks.

The Lay of the Land (Pun Intended!)

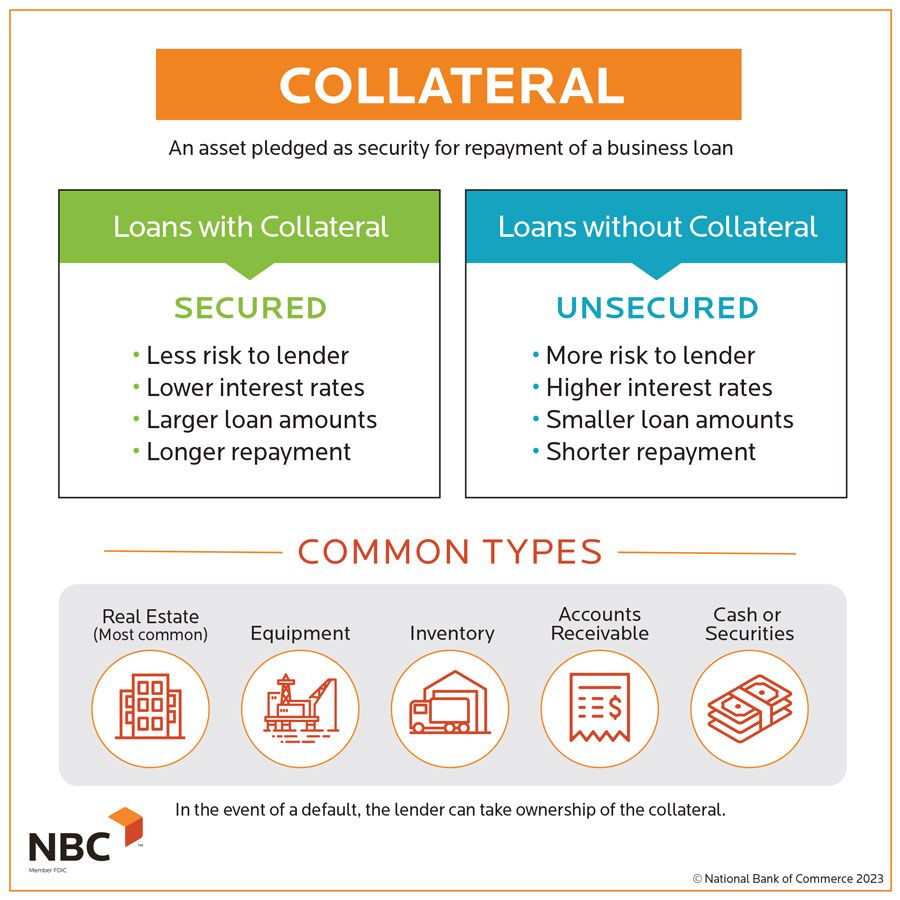

First things first: what exactly is a personal loan with land as collateral? Basically, it's a loan where you're using your property as a guarantee. If you can't repay the loan, the lender can take possession of the land. Think of it like that scene in "The Shawshank Redemption" where Andy Dufresne uses his rock hammer to slowly, painstakingly tunnel to freedom. Your land is the rock, the loan is the tunnel... except, hopefully, the repayment process is much faster and less... dramatic.

Now, let’s address the elephant in the room: bad credit. Having a less-than-perfect credit score can definitely make things trickier. Lenders see you as a higher risk, so they might charge higher interest rates or require even more stringent terms. It's like trying to get into a trendy club and the bouncer is giving you the side-eye. But don't lose hope! There are still options out there.

Must Read

Why Use Land as Collateral?

So, why would anyone use their precious land as collateral? Well, there are several reasons. Land often holds significant value, even if it's just a vacant lot. This value can allow you to borrow a larger amount than you might otherwise qualify for with just your credit score. Maybe you need funds for a business venture, home improvements (finally building that she-shed!), or consolidating existing debt. Using land can open doors that would otherwise be locked tight.

Another advantage is potentially securing a lower interest rate. Because the loan is secured by your land, the lender's risk is reduced. This can translate to better terms for you. It’s like ordering the premium coffee – it might cost a bit more upfront, but the long-term benefits (read: amazing flavor and productivity) can be worth it.

The Nitty-Gritty: What to Watch Out For

Okay, time for the real talk. Before you jump in headfirst, you need to be aware of the potential pitfalls. Foreclosure is the biggest risk. If you can't repay the loan, the lender can take your land. It’s crucial to be absolutely sure you can handle the repayment schedule. Think of it as planning a road trip: you need to map out your route, check your tires, and pack snacks. Repaying your loan is the successful arrival at your destination.

Also, pay close attention to the loan terms. What's the interest rate? Are there any hidden fees? What's the repayment schedule? Read the fine print carefully – like deciphering the lyrics to a mumble rap song. Don't be afraid to ask questions. This is your money and your land we're talking about!

Practical Tip #1: Shop around. Don't settle for the first lender you find. Get quotes from multiple sources and compare their terms. It's like dating – you wouldn't marry the first person you meet, would you? (Okay, maybe some people do, but you get the point.)

Practical Tip #2: Improve your credit score. Even a small improvement can make a big difference. Pay your bills on time, reduce your debt, and check your credit report for errors. It's like prepping for a marathon – every little bit of training helps.

Finding the Right Lender

So, where do you even start looking for a lender? Local banks and credit unions are a good place to begin. They often have more flexible lending criteria than larger national banks. Online lenders are another option, but be sure to do your research and check their reputation. It’s like finding a good food truck – read the reviews and make sure they haven't been shut down for health code violations.

Practical Tip #3: Consider a co-signer. If you have a friend or family member with good credit, they might be willing to co-sign your loan. This can significantly improve your chances of approval and potentially lower your interest rate. Just be sure they understand the risks involved.

Is It Right for You?

Ultimately, the decision of whether or not to take out a personal loan with land as collateral is a personal one. There's no one-size-fits-all answer. But it is crucial to ask yourself the hard questions: are you confident in your ability to repay the loan? Are you comfortable with the risks involved? Could you potentially find alternative financing options?

Think of your land as a prized possession – something to be protected and cherished. Only use it as collateral if you've carefully weighed the pros and cons and are confident that it's the right move for you.

Reflection: Financial decisions, especially those involving significant assets like land, can feel overwhelming. But by breaking down the process, understanding the risks, and seeking professional advice when needed, you can make informed choices that align with your goals. And remember, even when things get tough, there's always a way to tunnel to a brighter future, one carefully considered step at a time. Just maybe skip the rock hammer this time.