Should I Use My Credit Card To Build Credit

Okay, let's talk about something that makes most adults sweat: credit cards and building credit. Everyone always says you have to use a credit card to build credit. It's practically financial gospel. But here's my slightly rebellious, possibly unpopular opinion: maybe... maybe not?

Hear me out! I know, I know. You're picturing a credit score graph plummeting into the fiery pits of financial despair if you avoid plastic like the plague. We've all been there. But let's think about this rationally, while adding a pinch of humor. Because, honestly, stressing about credit scores can turn anyone into a grumpy cat.

The Credit Card Gospel: Debunked?

The standard advice goes something like this: "Get a credit card! Use it for small purchases! Pay it off every month!" It's like a financial mantra. Repeat it three times before bedtime and suddenly you're a responsible adult. Right? Maybe. But what if you're someone who... let's just say... enjoys spending? Like, really enjoys it?

Must Read

Because that tiny piece of plastic? It's not just a tool for building credit. It's also a tiny portal to a world of impulse buys, late-night online shopping sprees, and that "I deserve it!" mentality. And suddenly, "small purchases" become "slightly larger purchases" which then morph into "oh dear, I'm going to have to eat ramen for the next month."

I'm not saying everyone is like this. But let's be honest, for some of us, credit cards are less about building credit and more about feeding our inner shopping demons.

Alternatives? Gasp!

So, what's a financially responsible (or trying-to-be) person to do? Are we doomed to a life of credit score purgatory without the magical credit card? Fear not! There are other ways to prove you're a reliable human being who pays their bills.

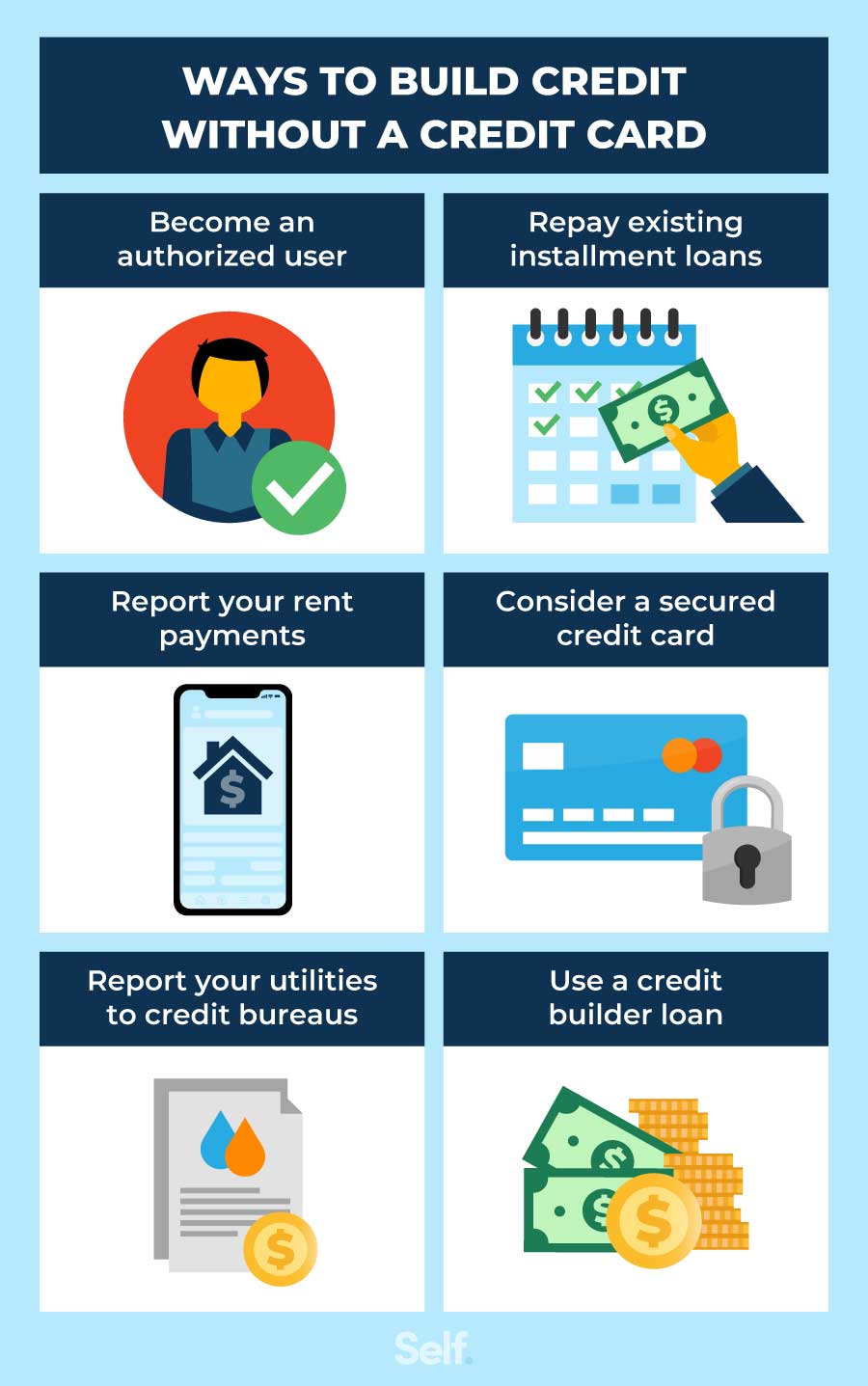

Ever heard of things like: Rent reporting services? Yep, you can get your on-time rent payments reported to credit bureaus. Finally, all those years of paying rent can actually work for you instead of just emptying your bank account! (It is important to verify which credit bureaus these services report to. It is not all of them.)

Or what about a secured credit card? This is a way to dip your toes into the credit card pool without diving headfirst. You basically put down a deposit, and that deposit becomes your credit limit. It is like a training wheel for credit. You can show you can responsibly manage a small amount of credit before jumping into the deep end.

And let's not forget credit-builder loans! These are specifically designed to help you build credit. You borrow a small amount of money, make regular payments, and bam! You're building credit. It's like a financial workout for your credit score.

The Unpopular Truth

Look, I'm not saying credit cards are inherently evil. They can be a useful tool if you can wield them responsibly. But if you're like me, and the temptation to splurge is strong, maybe exploring other credit-building options is the way to go. Maybe using a credit card to build credit is like trying to train a puppy with a steak in your hand. Sure, it could work, but it's probably going to be messy. So if you tend to struggle with that and are thinking, "Oh, I will just set up automatic payments.", just remember that those automatic payments still need to be funded.

Ultimately, the decision is yours. Weigh the pros and cons. Consider your own spending habits. And remember, a good credit score is important, but so is your sanity. Maybe that fancy latte isn't worth the potential credit card debt. Or maybe it is. I'm not judging.

"Do what's right for you. And maybe hide your credit card... just in case." - Someone (probably me)

Now, if you'll excuse me, I'm going to go hide my credit card. Just in case.