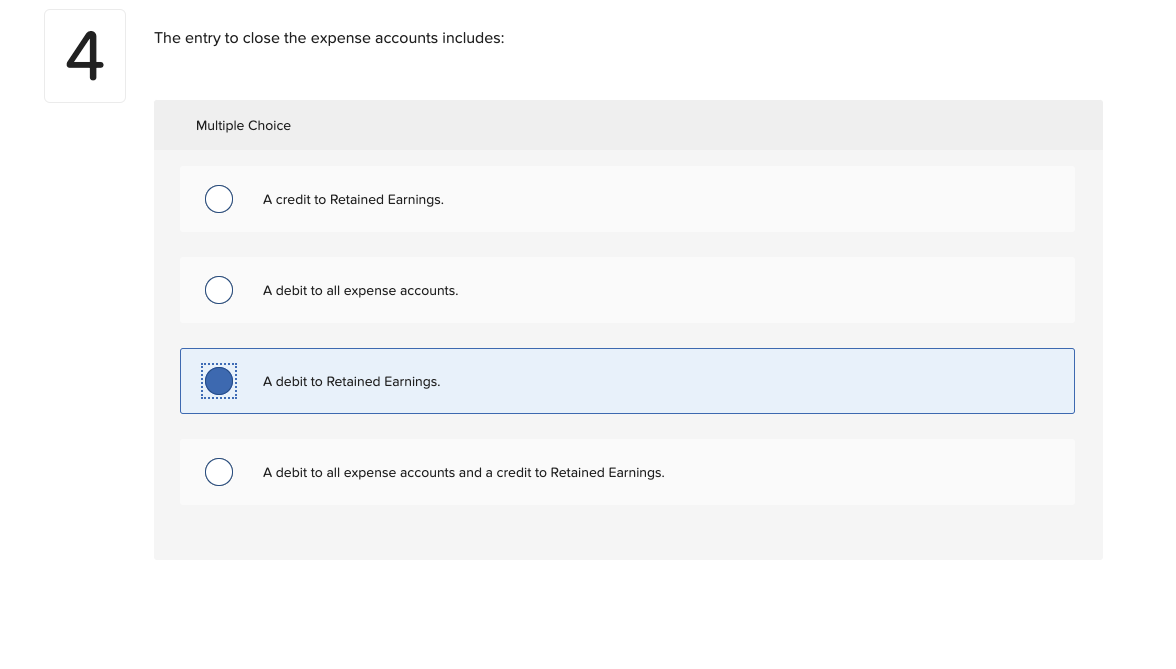

The Entry To Close The Expense Accounts Includes

Okay, let's talk about expense accounts. I know, I know, your eyes might be glazing over already. But stick with me! This isn’t about complicated accounting jargon; it’s about something that affects everyone, from freelancers sipping lattes in coffee shops to employees jetting off to conferences.

Think of expense accounts like your own personal reimbursement piggy bank. You spend money on behalf of your company (or your own business), and the goal is to get that money back. Easy peasy, right?

The Grand Finale: Closing the Expense Account

But what happens after you’ve submitted all your receipts, gotten your approval, and received your reimbursement? That’s where the “entry to close the expense accounts” comes in. It’s the final bow, the mic drop, the "ta-da!" of the whole expense process. It's where we essentially say, "Okay, this expense is settled. Let's clean it up in our accounting books."

Must Read

Imagine you’re baking a cake. You mix the ingredients, bake it to perfection, frost it beautifully, and finally… eat it! Closing the expense account is like that last satisfying bite. It's the culmination of all the hard work you put into tracking your expenses.

Why should you care? Well, proper closure ensures accuracy in your company's (or your own) financial records. It prevents double-counting, keeps things organized, and makes sure everything balances out nicely. Think of it as keeping your financial house in order. Nobody wants a messy house, right?

The Key Players in the Closing Act

So, what exactly does this "closing entry" involve? Don't worry, we’re not going to dive into a sea of debit and credit jargon. But here are the main components, in a nutshell:

- The Expense Account Itself: This is where the initial expense was recorded. Let's say you spent $100 on a client dinner. This account now has $100 sitting in it. We need to reduce this account to zero, essentially acknowledging that the company owes nothing on this expense.

- The Offset Account: This is usually either the cash account (if you've already been reimbursed) or an accounts payable account (if the reimbursement is pending). Think of it as the place where the money came from or will come from to cover the expense.

The Entry: The closing entry essentially moves the balance from the expense account to the offset account. In simple terms, it says, "The expense is no longer outstanding because it has been paid (or will be paid) from this other account."

Think of it like this: you borrowed $20 from a friend (the expense account). When you pay them back (the reimbursement), you no longer owe them that money. The debt is cleared! That's what the closing entry does – clears the "debt" in the accounting books.

Example Time!

Let's say Sarah took a client to lunch, and the bill came to $50. She paid for it out of pocket and submitted an expense report. Here's a simplified view of what happens:

- Initial Expense: The company records an expense of $50 (debit) to the "Client Meals" expense account and a corresponding credit to "Accounts Payable" (because they owe Sarah $50).

- Reimbursement: The company pays Sarah $50. They debit "Accounts Payable" (reducing what they owe Sarah) and credit "Cash" (because the money went out).

- Closing Entry: This might seem redundant, but it's crucial. The closing entry might not be a separate, visible transaction but it's a reconciliation happening within the accounting system. It ensures all parts of the transaction are in sync and the "Client Meals" expense is properly reflected in the financial reports. It's making sure all the t's are crossed and i's are dotted behind the scenes.

In this simplified example, the closing entry is more of an internal reconciliation within the accounting software, ensuring everything balances after the reimbursement. It is a crucial step for accurate financial reporting.

Why It Matters In The Real World

So, why should you, the average person, care about this seemingly technical stuff? Here are a few reasons:

- Accurate Financial Reporting: Proper expense account closure ensures that your company's financial statements are accurate. This is important for everything from securing loans to attracting investors.

- Preventing Fraud: While it might sound dramatic, sloppy expense management can open the door to fraud. Closing accounts correctly helps track expenses and identify any discrepancies.

- Better Budgeting: Accurate expense tracking allows companies to budget more effectively. Knowing where your money is going helps you make smarter financial decisions.

- Smooth Audits: If your company is ever audited, well-maintained expense records will make the process much smoother and less stressful.

Think of it as keeping your own personal budget. If you don't track your spending accurately, you might end up wondering where all your money went! The same principle applies to businesses. They need to know where their money is going, and closing expense accounts is a vital part of that process.

In conclusion, while the "entry to close the expense accounts" might sound like a dry accounting term, it’s a crucial part of ensuring accurate financial reporting, preventing fraud, and making informed business decisions. So next time you submit an expense report, remember that little closing entry working its magic in the background, keeping everything in tip-top financial shape!