The Optimal Capital Structure Has Been Achieved When The

Remember that time you tried to build the ultimate LEGO castle? You had all these cool bricks, but you were either short on the big, stable ones (equity, anyone?) or you went overboard with the flashy but wobbly ones (debt, oh debt!). The whole thing kept collapsing, right? That's kinda like a company trying to figure out its capital structure.

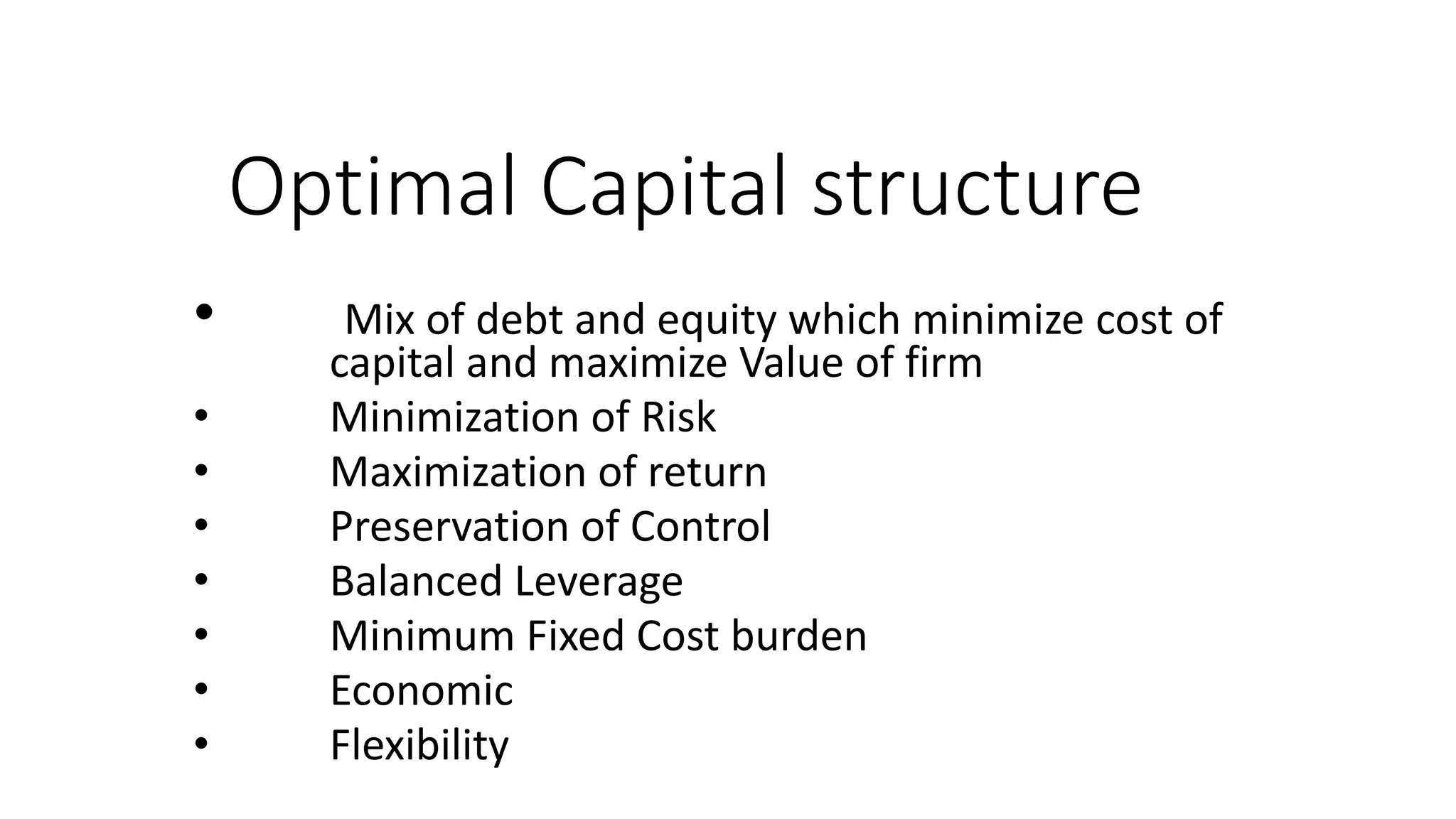

See, a company's "capital structure" is just how it funds its operations – a mix of debt (borrowing money) and equity (selling ownership). And finding the sweet spot, the optimal mix, is what every CFO dreams of.

So, When is the Magic Moment?

The optimal capital structure, in theory, is achieved when…

Must Read

…hold on to your hats…

…it maximizes the company's value. Yeah, it sounds obvious, doesn't it? But getting there is the tricky part. It's not about simply having the least amount of debt or the most amount of equity. It's about finding the perfect blend that makes the whole enterprise worth more than the sum of its parts. (Think synergy!)

Think of it like a recipe. Too much sugar (debt) and it's sickly sweet and unsustainable. Too much flour (equity, in this analogy, since it dilutes ownership) and it's bland and uninspired. The right proportions? Delicious!

What Maximizing Value Really Means (and Why It's Not Always Easy)

Okay, "maximizing value" is a bit of a buzzword. Let's break it down.

Essentially, a higher company value translates to:

- Higher stock price: Happy shareholders!

- Lower cost of capital: Easier (and cheaper!) to raise funds in the future.

- More investment opportunities: Because you're swimming in cash and investor confidence.

But achieving this is like trying to hit a moving target. Factors like market conditions, industry dynamics, and the company's own risk profile are constantly shifting the goalposts. (Seriously, the stock market is a fickle beast.)

A company's tax situation also plays a HUGE role. Debt interest is usually tax-deductible, which makes debt seem appealing. But too much debt can lead to financial distress, wiping out those tax benefits entirely. It's a delicate balancing act.

Side note: Did you know that companies in stable, predictable industries (like utilities) tend to carry more debt than companies in volatile, high-growth industries (like tech)? That's because they can more easily predict their future cash flows and service that debt.

The Trade-Off Theory: A Balancing Act of Benefits and Costs

One popular theory that tries to explain optimal capital structure is the Trade-Off Theory. It basically says that companies should borrow money up to the point where the tax benefits of debt are exactly offset by the costs of financial distress (like bankruptcy).

In other words, you want to squeeze every last drop of tax advantage out of debt, but you don't want to push it so far that you risk collapsing under the weight of your obligations.

Important: This isn't an exact science! There's no magic formula. It's all about making informed judgments based on the best available information.

Beyond the Numbers: Intangible Factors

While financial models and spreadsheets are essential, the optimal capital structure also involves considering some less tangible factors. Like…

- Management's risk tolerance: Are they bold and aggressive, or cautious and conservative?

- Investor sentiment: What are investors comfortable with? What are they demanding?

- Flexibility: Does the capital structure allow the company to respond to unexpected opportunities or challenges?

Ultimately, finding the optimal capital structure is a continuous process of analysis, adjustment, and re-evaluation. It's not a destination, it's a journey. And just like that LEGO castle, it might need some tweaking along the way to stay strong and stable.

So next time you're building something, remember that the same principles apply to finance! (Okay, maybe not exactly the same, but the core idea of balance and optimization is there.)