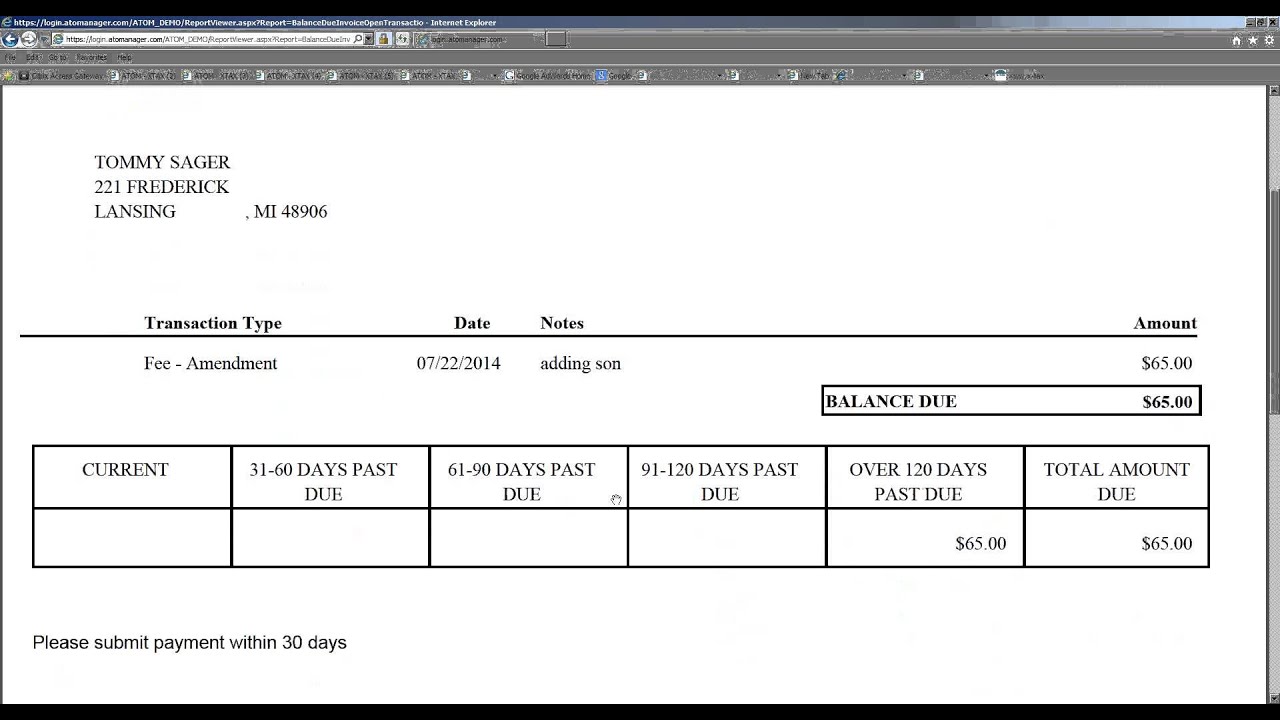

The Total Amount Owed Does Not Reflect This Pending Payment.

Ever gazed at your bank statement or credit card bill and thought, "Wait a minute, that number doesn't quite add up to what I thought I owed!"? You're not alone! It's a common moment of mild panic, often followed by seeing that little phrase: "The total amount owed does not reflect this pending payment." Instead of a headache, let's turn this into a fun little financial detective game. Understanding this seemingly complex banking jargon is incredibly useful, making your everyday money management smoother and giving you a wonderful sense of control. It’s like knowing the secret handshake to navigate your finances with confidence!

So, what’s the big deal about "pending payments" and why should you care? Well, it offers big benefits for all sorts of folks! For beginners just starting to manage their own money, grasping this concept is foundational. It teaches you that not all transactions hit your account instantly, saving you from confusion and potential overdrafts. For busy families, it's a lifesaver for budgeting. Imagine you've just done the weekly grocery shop and paid a big bill; knowing that the money isn't gone from your bank balance just yet, but is earmarked, helps prevent accidental overspending on other items. And even for casual hobbyists, say, someone planning a big trip or collecting rare items online, it helps you keep a real-time pulse on your spending, ensuring you stick to your budget without nasty surprises from delayed transactions.

Let's look at some common scenarios where this phrase pops up. Think about your credit card statement. You might have made a payment yesterday, but it hasn't "posted" yet, meaning the credit card company hasn't officially processed it. The statement balance still shows the old, higher amount, but your actual obligation has already changed. Or consider your debit card. When you fill up your car with gas or check into a hotel, they often put a "hold" or "pending charge" on your account for a slightly higher amount than you expect, just in case. The money isn't truly gone, but it’s temporarily unavailable. Your bank’s online portal might show an "available balance" that already accounts for these pending items, while the "current balance" does not. It's a subtle but crucial difference!

Must Read

Ready to become a financial guru? Here are some simple, practical tips to get started. First, always check your available balance, especially before making a big purchase. This number typically reflects what you really have left after pending transactions are factored in. Second, consider keeping a simple, personal record – even a quick note on your phone – of recent transactions you’ve made, especially those you know will take a day or two to process. This creates your own "pending" tracker. Third, understand the difference between pending and posted. A pending transaction is authorized and awaiting finalization, while a posted transaction is complete and reflected in your main balance. Finally, many banks offer text or email alerts for transactions. Setting these up can give you real-time notifications, helping you keep tabs on your money without constant checking.

By taking a few minutes to understand this little financial quirk, you're not just avoiding confusion; you're gaining empowerment. It transforms a potential moment of stress into an opportunity for greater financial clarity and control. You'll enjoy the peace of mind that comes from truly knowing where your money stands, making your everyday financial journey not just smoother, but genuinely more enjoyable!