Utility Self Reported On Credit Report

Okay, let's talk about something that might not sound super exciting at first glance, but trust me, it's like finding a twenty-dollar bill in your old jeans – a pleasant surprise! We're diving into the world of utility bills and your credit report. Specifically, how reporting those bills can actually boost your credit score. Yep, you heard that right. Paying your electricity and gas could be your secret credit-building weapon!

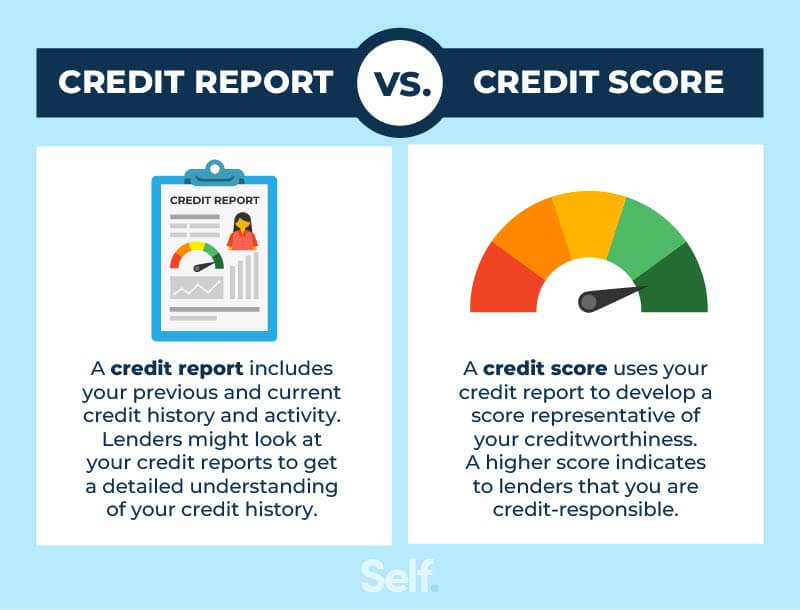

Think of your credit report like your financial reputation. It tells lenders (banks, credit card companies, etc.) how reliable you are when it comes to paying back money. A good credit score opens doors – lower interest rates on loans, better credit card offers, even easier approvals for renting an apartment. So, anything that helps improve that score is definitely worth exploring.

What's "Utility Self-Reporting?"

So, what exactly is utility self-reporting? It's basically when you, the consumer, take the initiative to have your on-time utility payments added to your credit report. Traditionally, only things like credit cards, loans (car loans, mortgages, student loans), and sometimes rent payments show up. But, the world is changing! And you can now get your utility companies to report your payment history, too.

Must Read

Imagine you're baking a cake. Traditionally, you only add flour, sugar, and eggs (representing credit cards, loans, etc.). Utility self-reporting is like adding a secret ingredient – a little vanilla extract – that enhances the flavor and makes it even better! It's an extra layer of positive information showing you're responsible with your finances.

Why Should You Care? (Hint: It's About More Than Just Bragging Rights)

Here's the thing: millions of people pay their utility bills on time every single month. They're proving their financial responsibility without getting any credit (pun intended!) for it. Utility self-reporting allows you to get the credit you deserve.

It's especially helpful if you have a thin credit file. A "thin file" simply means you don't have a lot of credit history. Maybe you're young, or maybe you haven't used credit much in the past. Utility self-reporting can provide a significant boost, adding positive payment history where there was little before.

Even if you have an established credit history, adding utility payments can still help. It diversifies your credit profile, showing lenders you're responsible with different types of bills. Think of it as showing off your well-rounded financial skills!

Let’s say you are rebuilding credit after some financial challenges. You've diligently paid your utility bills on time for the past year. By self-reporting those payments, you can demonstrate your commitment to responsible financial behavior and potentially offset some of the negative marks on your credit report.

How Do You Actually Do It?

This is where things can get a little tricky, as not all utility companies report to the major credit bureaus (Equifax, Experian, and TransUnion). But don't worry, it's not rocket science! Here's the general process:

- Contact your utility providers. Call them (or check their website) and ask if they report to credit bureaus. Some may already do so automatically, but most likely they do not.

- If they don't directly report, look into third-party reporting services. Companies like Experian Boost (yes, one of the credit bureaus offers this) and UltraFICO allow you to link your bank accounts and have your utility payments (and sometimes even streaming services like Netflix!) factored into your credit score.

- Be prepared to provide information. You'll likely need to provide your account information, authorization to access your bank statements, and consent for the service to report your payment history.

Important Note: Make sure to research any third-party service before signing up. Read reviews, understand their fees (if any), and make sure their data security practices are solid.

Potential Downsides (Yes, There Are a Few)

While utility self-reporting is generally a good thing, there are a few potential downsides to be aware of:

- Missed payments can hurt your score. If you consistently pay your utility bills late, self-reporting could actually lower your credit score. So, make sure you're on top of your payments!

- Not all lenders use this information. Some lenders may not give as much weight to utility payments as they do to traditional credit accounts.

- Potential fees. Some third-party services may charge fees for their reporting services. Weigh the costs against the potential benefits.

Consider it like this: you want to show off your amazing homemade cookies (your financial habits), but you accidentally burn a batch (missed payment). That burnt batch might not look so appealing! So, make sure your cookies are perfect (payments are on time) before showing them off.

The Bottom Line

Utility self-reporting is a relatively new and evolving concept, but it can be a valuable tool for building or improving your credit score, especially if you have a thin credit file or are rebuilding your credit. Do your research, weigh the pros and cons, and decide if it's right for you. After all, every little bit helps when it comes to building a strong financial foundation. Now go forth and get credit for those on-time utility payments!