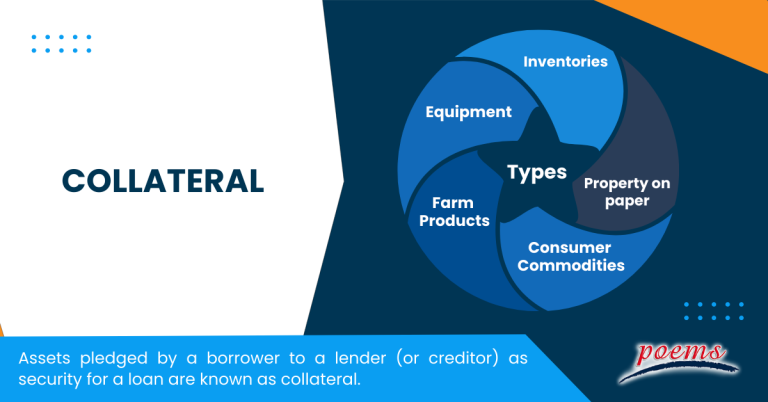

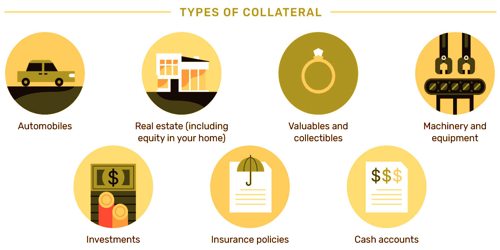

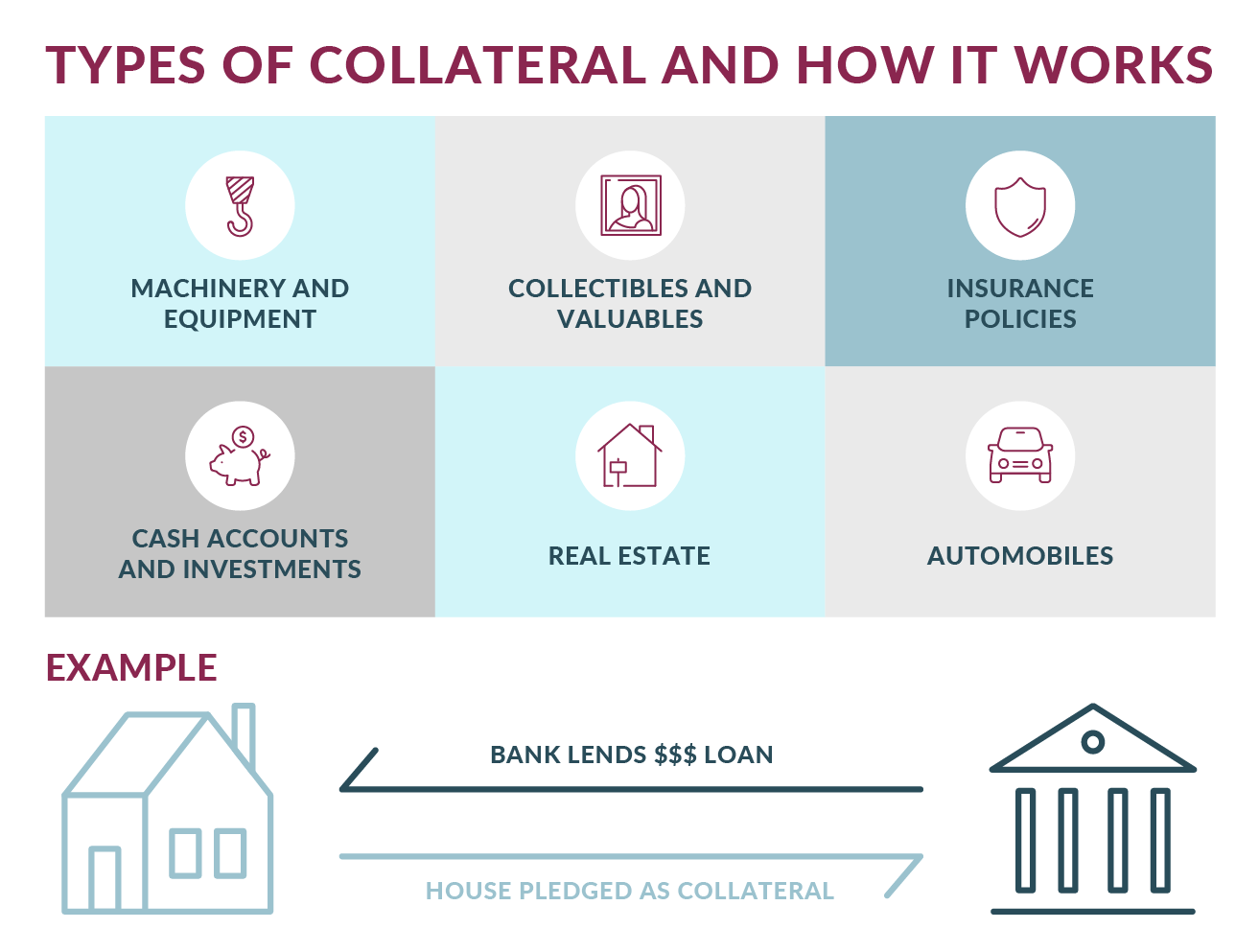

What Are The Five 5 Types Of Collateral

Ever wondered how banks decide who gets a loan and who doesn't? It's not just about your charming personality (though that probably helps!). A big piece of the puzzle is something called collateral. Think of it as a safety net – something valuable you offer up as a guarantee that you'll repay what you borrow. Sounds a bit serious, right? But understanding the different types of collateral is surprisingly interesting and useful, whether you're dreaming of starting a small business, buying a house, or just want to be financially savvy. Let's dive in!

So, what are these mystical five types of collateral? Here's a friendly breakdown:

1. Real Estate: This is probably the most familiar type of collateral. Think of your house, apartment, or even land. If you take out a mortgage, the property itself acts as collateral. If you fail to make your payments, the lender can foreclose and sell the property to recoup their money. For families looking to buy their dream home, understanding this is crucial! It highlights the importance of responsible borrowing and budgeting.

Must Read

2. Cash and Securities: This category includes savings accounts, certificates of deposit (CDs), stocks, and bonds. These are relatively liquid assets, meaning they can be easily converted to cash. A beginner investor might use their stock portfolio as collateral for a loan, allowing them to leverage their existing investments. However, it's important to understand the risks involved, as the value of these assets can fluctuate.

3. Equipment: This is common for businesses, especially those that rely on specific machinery or technology. Examples include manufacturing equipment, vehicles, or even computer systems. A small business owner might use their delivery truck as collateral for a loan to expand their operations. This is a great way to finance growth, but remember that the lender will assess the value and condition of the equipment.

4. Inventory: Similar to equipment, inventory (raw materials, work-in-progress, or finished goods) can be used as collateral, particularly for retail businesses. Imagine a clothing store using its stock of clothes as collateral. While this can be a helpful option, the lender will carefully evaluate the marketability and perishability of the inventory.

5. Accounts Receivable: This refers to the money owed to a business by its customers. In essence, the business is using the future payments from its clients as collateral. This can be a useful financing tool for businesses that have a strong and consistent customer base.

Tips for Getting Started (Thinking About Collateral):

- Know Your Assets: Make a list of everything you own that could potentially be used as collateral.

- Understand the Risks: Before pledging any asset as collateral, carefully consider the consequences of default.

- Shop Around: Different lenders have different requirements and may value your collateral differently.

Understanding the five types of collateral isn't just about loans and finances; it's about knowing the value of what you have and making informed decisions. Whether you're a budding entrepreneur or simply managing your family's finances, this knowledge can empower you to achieve your goals with confidence. So, go forth and explore the world of collateral – it's more interesting than you might think!

:max_bytes(150000):strip_icc()/collateral-9d1d0360292b4a06989957c5e3239fb5.jpg)