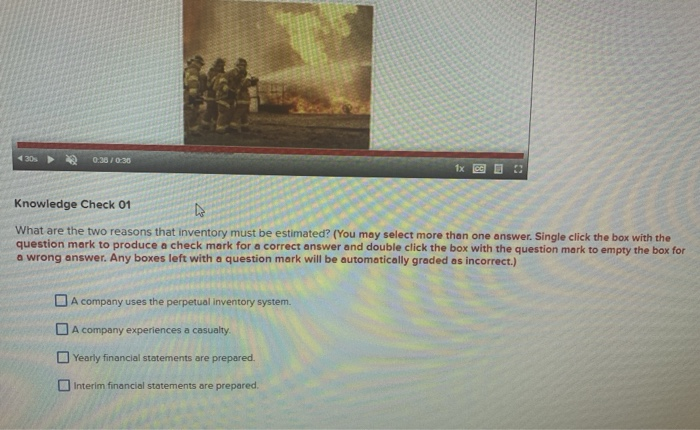

What Are The Two Reasons That Inventory Must Be Estimated

Okay, let’s talk about something that sounds super boring – inventory estimation. But trust me, it's way more relatable than you think. Imagine you’re planning a potluck. You swear you bought enough chips, but then Aunt Mildred brings her famous seven-layer dip (again!), and suddenly, everyone’s inhaling chips like it’s their last meal. You need to figure out, quick, if you need a chip run! That’s kind of like inventory estimation. Except, you know, with less seven-layer dip drama.

Reason #1: Uh Oh, We Goofed! (Or, "Houston, We Have a Fire Sale…Literally!")

The first reason we need to estimate inventory is because sometimes…things don't go according to plan. Think of it like this: you’re baking cookies for a bake sale. You meticulously counted out 100 chocolate chips per cookie. Then your dog, Sparky, leaps onto the counter, devouring half a bag of chocolate chips and knocking over a bowl of flour in the process. Now your kitchen looks like a winter wonderland, and your chocolate chip count is, shall we say, compromised.

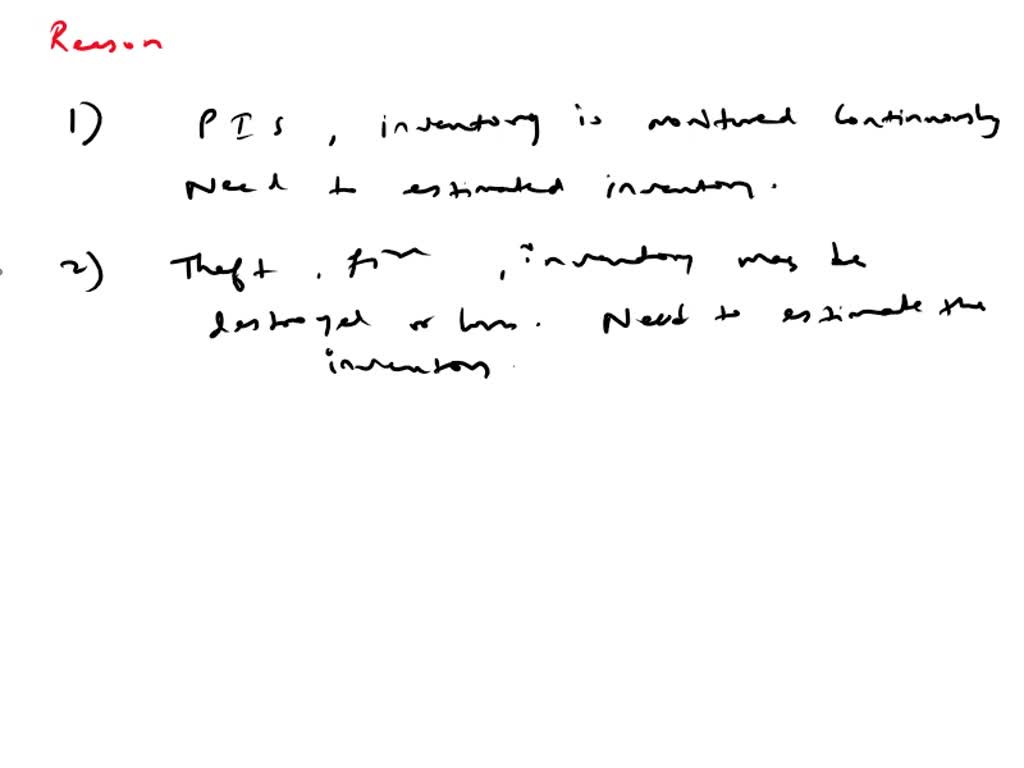

In the business world, this “Sparky” situation can take many forms. Maybe there was a fire (hopefully not!), a flood, or some other type of natural disaster. Imagine trying to count inventory after a hurricane! Good luck with that. Or, maybe there was some good old-fashioned theft. Yep, someone might have walked off with a pallet of your limited-edition garden gnomes (hey, it could happen!). These unforeseen circumstances make it impossible to do a physical count. That's when inventory estimation swoops in like a superhero, or at least a very organized accountant.

Must Read

The key here is that a physical count is either impossible or impractical. We need a quick and dirty way to figure out what should be there, based on what we know was there and what should have happened since. Think of it as detective work, only instead of solving a crime, you're solving an inventory puzzle. It's all about piecing together the clues to arrive at a reasonable estimate. This is when the methods like gross profit method or retail inventory method shine!

Reason #2: Interim Financial Statements (Or, "Are We Profitable Yet?")

The second big reason for estimating inventory is for preparing interim financial statements. These are basically financial reports done before the end of the year. Think of it like checking your bank account balance halfway through the month to see if you can afford that new gadget. Companies do the same thing, but on a much larger scale. They need to know, “Are we making money? Are we losing money? Should we panic and sell all the garden gnomes?”

Now, doing a full physical inventory count is time-consuming and expensive. Imagine shutting down your entire warehouse just to count every single widget! It's like stopping your potluck halfway through to count every single chip left in the bag. Nobody has time for that! It disrupts operations and can cost a fortune in lost productivity. Plus, who wants to miss Aunt Mildred’s seven-layer dip demolishing performance?

So, to create these interim reports without grinding everything to a halt, we estimate inventory. This allows companies to get a reasonable snapshot of their financial performance without the hassle of a full-blown physical count. These estimates will later be adjusted once the year end numbers are available. It is kind of like getting a health checkup. The final report is after all the blood results are available.

In summary, inventory estimation isn't just some obscure accounting trick. It's a practical tool that helps businesses deal with unexpected events and keep track of their performance throughout the year. Whether it's recovering from a chocolate chip-related kitchen disaster or trying to figure out if you can afford to expand your garden gnome empire, sometimes you just need a good estimate. Remember, accuracy is important but having a reasonable guess is better than not knowing at all! Now, back to those chips...