What Paperwork Is Needed To Buy A House

Alright, pull up a chair, grab a latte (venti, obviously, because we're talking about buying a HOUSE!), and let's chat about the paperwork involved. Think of it as climbing Mount Paperwork, but instead of oxygen tanks, you'll need a bottomless supply of ink and the patience of a saint.

Pre-Approval: The Paperwork Pep Rally

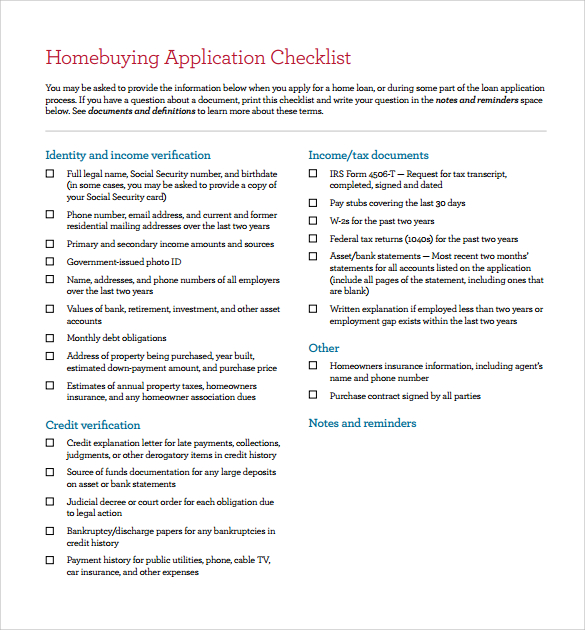

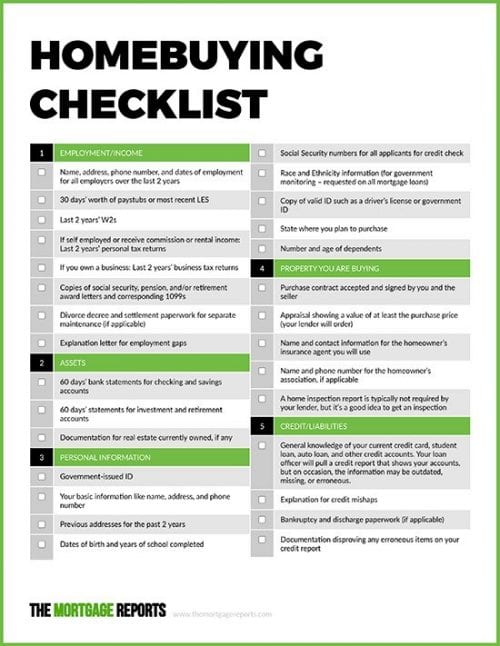

First, before you even think about falling in love with a charming Victorian or a modern glass box, you need to get pre-approved for a mortgage. This is basically showing the bank you’re serious (and solvent-ish). Imagine going on a date and having to prove you can afford the appetizers. Charming, right? Here’s what they’ll likely ask for:

- Proof of Income: Pay stubs, W-2s, tax returns – the whole shebang. Prepare to dive into your financial past like Indiana Jones searching for the Ark of the Covenant, only instead of snakes, you'll be facing receipts from that questionable late-night pizza order.

- Bank Statements: They want to see where your money lives, how it behaves, and if it's hiding any embarrassing secrets (like a crippling online shopping addiction).

- Credit Report: This is your financial GPA. Hopefully, it's not a D- because you forgot to pay your library fines… again. You can usually get a free copy online, so don't panic!

- ID: Driver's license, passport – something that proves you're actually you and not a sophisticated robot programmed to acquire real estate.

Fun Fact: Did you know some lenders will ask for a "letter of explanation" if they see any large deposits? Like if Grandma decided to gift you a small fortune, you’ll need to explain that it wasn't from a "suspicious source" – which, let’s be honest, Grandma's generosity is kind of suspicious. What's she hiding?!

Must Read

The Offer: "I Think I'm In Love" (With This House)

Okay, you’ve found "The One." The house, I mean. Hopefully, you also have "The One" in your personal life, but that's a whole different pile of paperwork (and possibly a prenup!). Now you need to make an offer. This involves even MORE paper, naturally.

- The Offer to Purchase: This is the big one! It details the price you're offering, the closing date you're hoping for, and any contingencies you want to include. Contingencies are basically your "get out of jail free" cards, like an inspection contingency (allows you to back out if the inspection reveals major issues) or a financing contingency (allows you to back out if you can't get a mortgage).

- Earnest Money Deposit: This is a good faith deposit you put down to show you're serious. It's like putting a ring on the house...a temporary ring made of cash.

- Disclosures: The seller has to disclose anything they know about the property, like if the basement floods every spring or if the house is haunted by a grumpy ghost who hates reality TV.

Pro-Tip: Read the fine print! I know, I know, it's boring, but that fine print can save you from buying a house with a colony of bats living in the attic (unless you're into that sort of thing).

Under Contract: Prepare for the Paper Blizzard

The seller accepted your offer! Woohoo! Now the real fun begins. It’s time for the under contract phase, which basically means "prepare to be buried alive in paperwork."

- Appraisal: The lender will order an appraisal to make sure the house is actually worth what you’re paying for it. Imagine a house wearing too much makeup trying to pass for younger than it is. That’s what the appraiser is trying to uncover.

- Inspection: This is where a professional inspector comes in and gives the house a thorough once-over. They’ll check for everything from termites to leaky faucets to that aforementioned grumpy ghost.

- Title Search: A title company will research the history of the property to make sure there are no outstanding claims or liens. You don’t want to buy a house only to find out that someone else still owns it, or that there's an undiscovered oil well on the property that belongs to your neighbor (although, that would be kind of cool).

- More Financial Documents: The lender will likely ask for updated versions of everything you already gave them, just to make sure you haven't suddenly decided to become a professional competitive eater and spent all your money on hot dogs.

Surprising Fact: Some lenders require you to provide documentation for every large deposit, even the legitimate ones. So, that $20 you won in the office lottery? Prepare to explain where it came from. It's like they think you're running a sophisticated underground bingo ring!

Closing: The Paperwork Finale (Hallelujah!)

You’ve made it! You’ve conquered Mount Paperwork! Now, for the grand finale: the closing. Prepare to sign your name approximately 7,432 times.

- The Deed: This is the official document that transfers ownership of the property to you. It’s like getting a marriage certificate, only instead of saying "I do," you're saying "I promise to pay my mortgage on time (or else!)."

- The Mortgage Documents: This is the agreement you’re making with the lender to borrow money to buy the house. It’s a long and complicated document filled with legal jargon, so don’t be afraid to ask questions.

- Closing Disclosure: This document details all the costs associated with the closing, including the purchase price, loan amount, closing costs, and taxes. Prepare to be shocked by the sheer amount of money involved.

Final Thought: Buying a house is a marathon, not a sprint. It requires patience, perseverance, and a healthy sense of humor. So, stock up on coffee, find a good real estate agent, and get ready to sign your life away (in a good way!). And remember, someday you'll be telling this story to your friends over lattes in your new living room!