What's Needed To Purchase A Home

Okay, picture this: You're curled up on the couch, maybe with a cup of tea (or something stronger, no judgment here!), binge-watching another episode of Property Brothers. They're talking about open-concept living, granite countertops, and how this couple's dream home is just waiting for them. You sigh, a little wistfully, and think, "Man, I wish that was me." We've all been there, haven't we? Dreaming of that perfect little (or not-so-little) slice of heaven to call our own. But then, the real world taps you on the shoulder and asks, "Uh, excuse me, but do you have a few hundred thousand dollars just lying around?" And suddenly, the dream feels a million miles away.

That's often the disconnect, right? The glorious vision versus the gritty reality of what it actually takes to get those keys in your hand. So, let's pull back the curtain, shall we? Because buying a home, while incredibly rewarding, isn't just about finding the right paint color. It's about a few key ingredients that, frankly, nobody really talks about enough in those feel-good TV shows. Spoiler alert: it’s mostly about money.

The Down Payment: Your Big Introduction

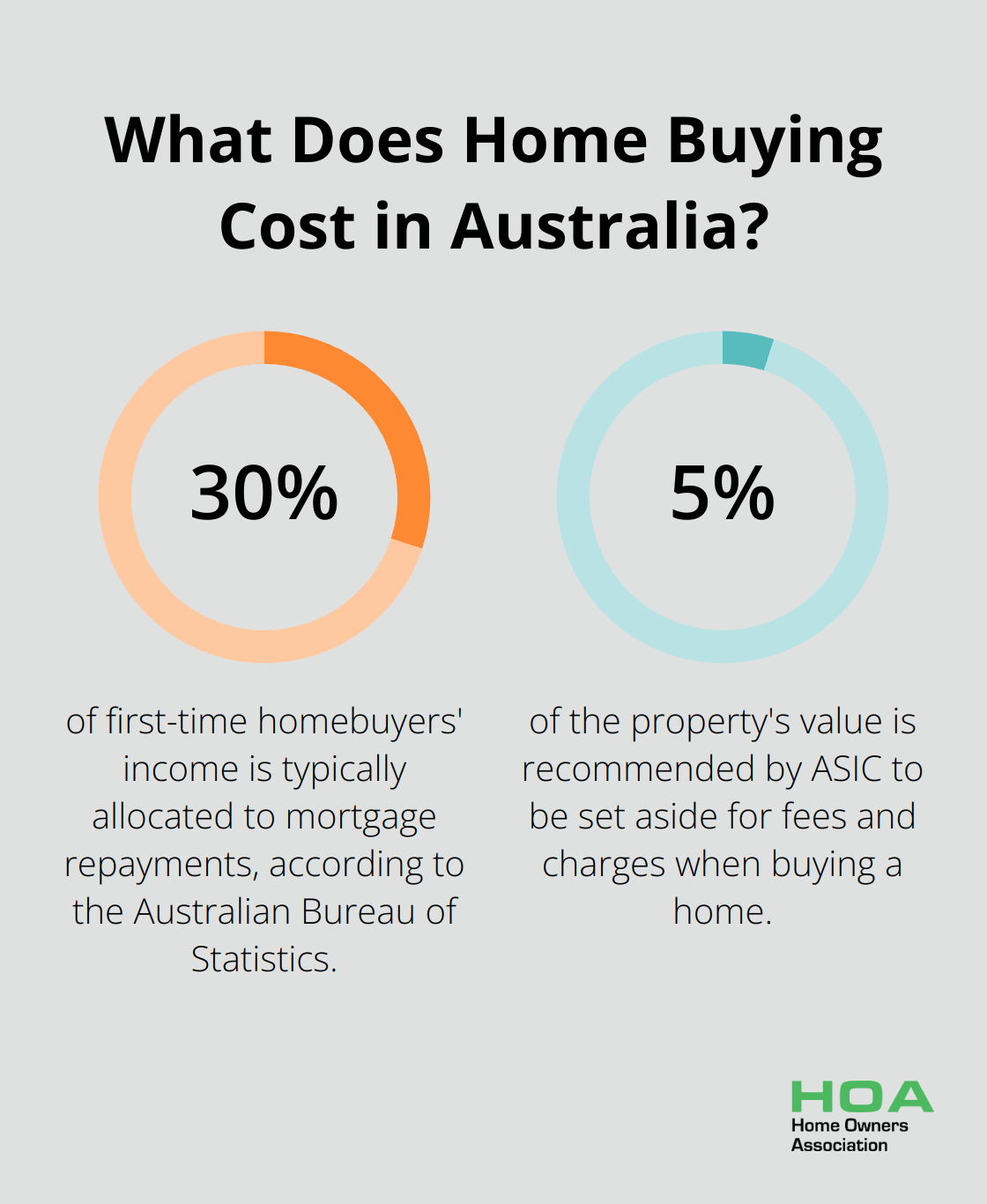

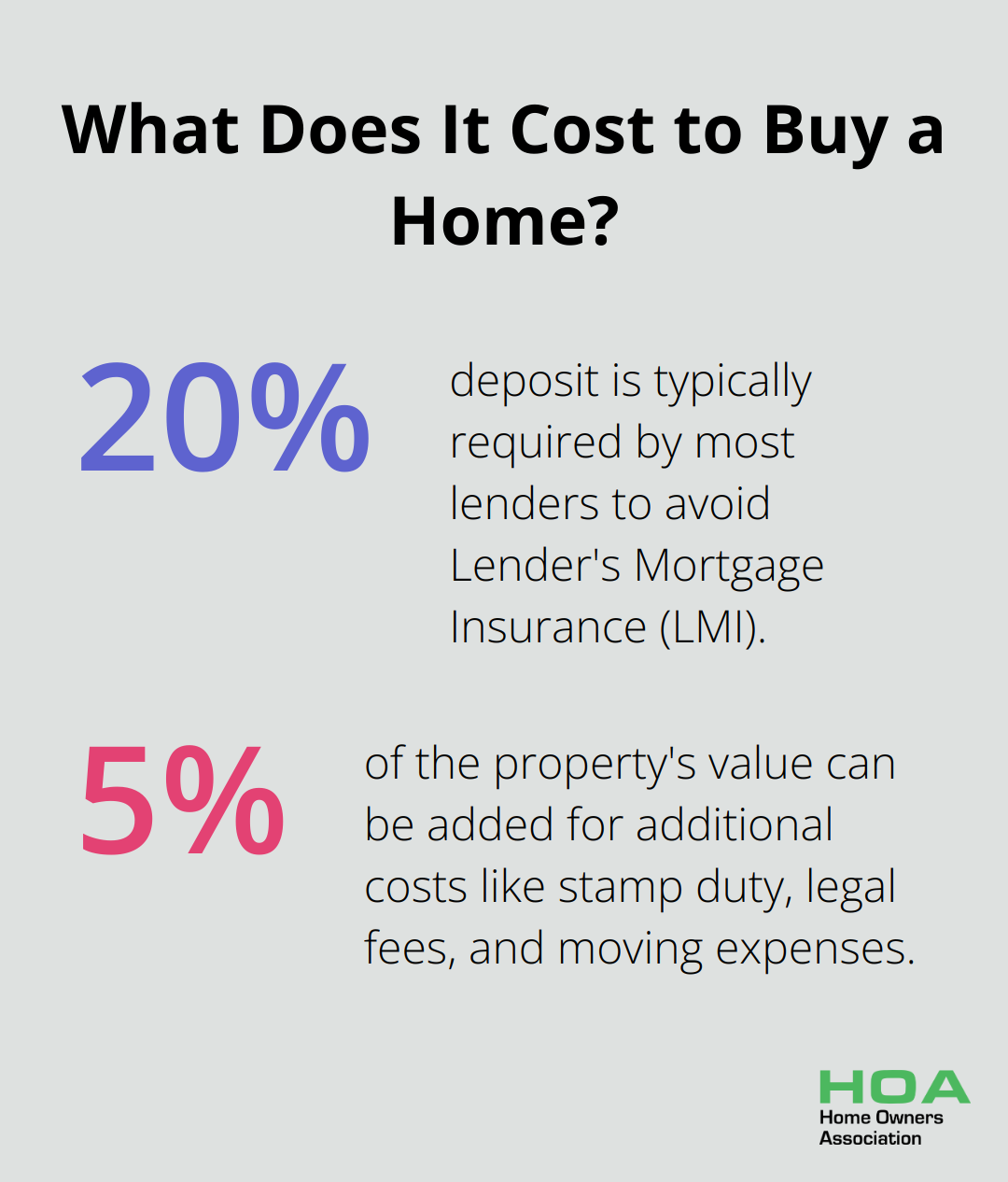

Let's start with the elephant in the room: the down payment. This is basically the chunk of money you pay upfront for your house. It shows lenders you're serious and helps reduce the amount you need to borrow. Everyone always talks about 20%, and yeah, that's kinda the gold standard because it usually means you avoid Private Mortgage Insurance (PMI), which is just extra money out of your pocket each month. But here’s the thing, 20% isn't always mandatory! There are programs out there for 5%, 3.5% (hello, FHA loans!), or even 0% for certain buyers (looking at you, VA loans). The catch? A smaller down payment usually means a bigger monthly payment and potentially that pesky PMI. So, start saving, my friend. Like, yesterday.

Must Read

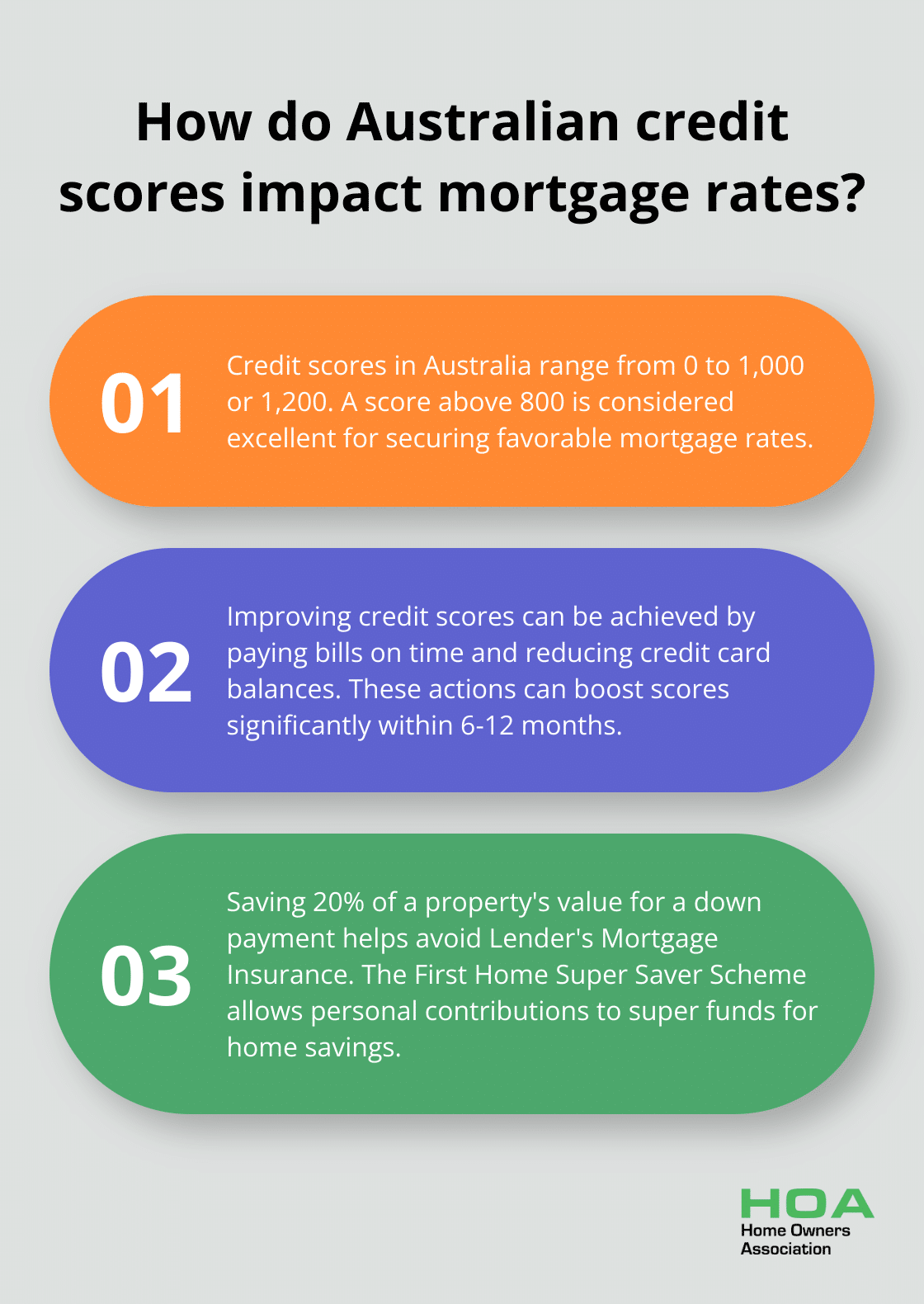

Your Credit Score: The Gatekeeper

Think of your credit score as your financial report card. When you apply for a mortgage, lenders are going to pore over this thing like it's the last page of a thrilling mystery novel. A higher score tells them you're a responsible borrower, making you look less risky and, crucially, qualifying you for better interest rates. And trust me, a better interest rate can save you tens of thousands of dollars over the life of a loan. So, pay your bills on time, keep your credit utilization low, and maybe don't open five new credit cards just before you plan to buy. It's all about demonstrating reliability, you know?

Income & DTI: Can You Actually Afford It?

This one's pretty straightforward, but often overlooked. Lenders want to see stable income. Like, a W-2 or solid self-employment history for a couple of years. They're checking your Debt-to-Income (DTI) ratio – basically, how much of your gross monthly income goes towards paying debts. If your DTI is too high, it signals that you might be stretched too thin, making you a higher risk. You’ll hear numbers like 43% as a common limit, but this can vary. So, time to crunch some numbers. What are your monthly payments for student loans, car loans, credit cards? The less debt you carry, the more house you can realistically afford. It's not just about what the bank approves, but what you can comfortable handle without eating ramen every night. (Unless you love ramen, then carry on!)

Those Pesky Closing Costs: The Hidden Surprises

Just when you think you’ve saved enough for the down payment, BAM! Here come closing costs. These are all the fees associated with finalizing your mortgage and transferring ownership of the property. We're talking appraisal fees, loan origination fees, title insurance, legal fees, recording fees, and a whole bunch of other fees that sound like they were made up on the spot. They typically range from 2-5% of the loan amount, and yes, you usually need to pay these upfront at closing. Don't let them catch you off guard! Factor these into your savings plan from day one.

Pre-Approval: Your Golden Ticket (Almost)

Before you even start touring open houses and falling in love with a kitchen you can't afford, get pre-approved for a mortgage. This isn't just a "nice to have," it's practically a necessity in today's market. A pre-approval letter from a lender shows sellers that you’re a serious, qualified buyer and not just a weekend browser. It tells them (and you!) exactly how much house you can afford, saving you from heartbreak later. Plus, it streamlines the actual loan process once you find "the one." Consider it your VIP pass to serious house hunting.

The Intangibles: Patience & A Good Team

Finally, let's talk about the stuff you can't put a price tag on. Buying a home is a journey, not a sprint. It requires patience – for the right house, for the paperwork, for the market fluctuations. And you'll need a good team: a fantastic real estate agent who understands your needs, a responsive lender who communicates clearly, and maybe even a supportive friend or partner to vent to when things get stressful. Because, let’s be real, it will get stressful. But with the right preparation and the right people in your corner, that dream home moves from the TV screen to your reality. You've got this!