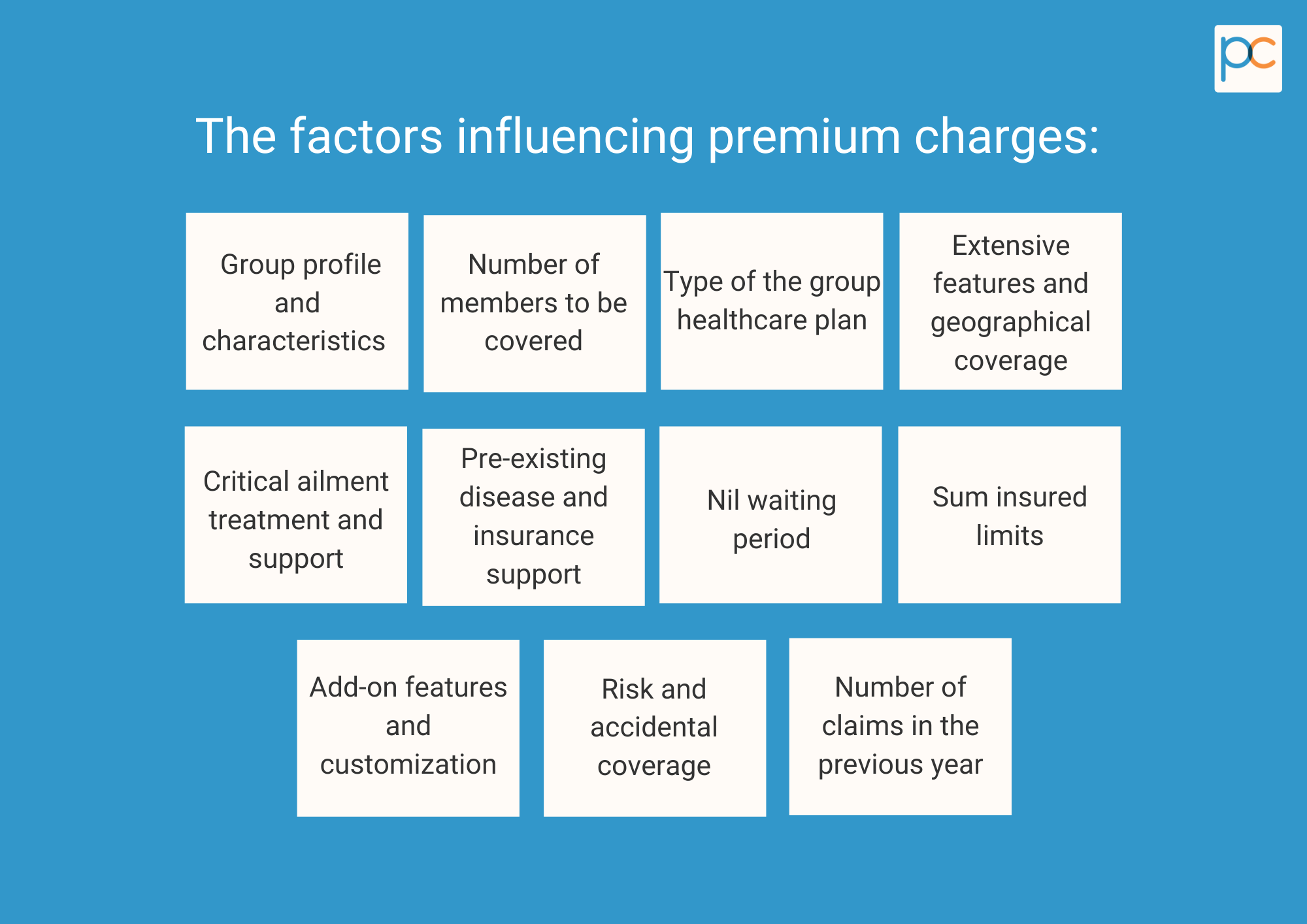

Which Of These Factors Would An Insurer Consider

:max_bytes(150000):strip_icc()/calculating-premium.asp_sketch_revised-5eb88ace64ae40cfa39d93ba9a23f19c.png)

Ever wondered what goes on behind the scenes when you apply for insurance? It's not some mysterious black box! Insurers actually look at a bunch of different things to figure out your risk level (and therefore, your premium). Let's demystify it, shall we? Think of it as unlocking a superpower – understanding how insurance works! It's way more exciting than it sounds, trust me.

Your Age: It's Just a Number (But Insurers Notice!)

Okay, let's start with the obvious: age. Generally (and I stress generally), younger folks might pay a bit more for car insurance because, statistically, they're newer drivers with less experience. But hey, don’t despair, young blood! With safe driving habits, that premium can come down faster than you can say "deductible." And for health insurance, age can play a role there too as older age groups have a higher probability of needing more care.

Location, Location, Location! (It's Not Just Real Estate)

Where you live makes a huge difference. If you're in a bustling city with lots of traffic and potential hazards (think: fender benders, higher crime rates), your car insurance might be higher. Similarly, if you live in an area prone to natural disasters (hurricanes, earthquakes, etc.), your home insurance will reflect that. Rural areas often enjoy lower premiums. So, while you can't exactly pack up and move just for cheaper insurance (unless you really want to!), it's definitely something to keep in mind.

Must Read

Your Driving Record: Honesty is the Best Policy (and Saves Money!)

This one's pretty straightforward: if you have a history of accidents or traffic violations, your car insurance is going to be higher. Insurers see you as a higher risk. It’s simple math. A clean record, on the other hand, is like a golden ticket! Think of it as insurance karma – good driving habits come back to reward you. This also applies to other types of insurance, where past claims are tracked. For example, home insurance claim history.

Health History: Your Body's Story (the Cliff's Notes Version)

When it comes to health insurance, your medical history is a key factor. Pre-existing conditions (things you've been diagnosed with before applying for insurance) can influence your premiums or coverage. However, there are regulations and laws (like the Affordable Care Act in the US) that protect people with pre-existing conditions. It's all about balancing risk and ensuring everyone has access to healthcare. Insurers can use your medical history to predict how much future care will cost them.

Lifestyle Choices: The Fun Stuff (and the Risky Stuff)

This is where things get interesting! Insurers might consider lifestyle factors like smoking, hobbies, and even your occupation. Smokers typically pay more for health and life insurance because of the increased health risks. And if you're a professional skydiver (talk about an adrenaline rush!), you might find your life insurance premiums are a bit higher than someone who enjoys, say, competitive knitting. (No offense to competitive knitters – I'm sure that's thrilling in its own way!). Your occupation is a measure of how risky your lifestyle is. For instance, if you drive for a living, you are at a higher risk of filing a car accident.

Credit Score: Not Just for Loans!

Believe it or not, your credit score can affect your insurance premiums in some areas (check your local regulations, as this isn't universally applied). Insurers argue that a good credit score indicates financial responsibility, which correlates with lower risk. So, keeping your credit in tip-top shape isn't just good for loans; it can also save you money on insurance! It helps insurance companies figure out the likelihood that you will pay premiums on time.

Coverage Choices: Deductibles and Limits (You're in Control!)

You have a say in how much you pay! Choosing a higher deductible (the amount you pay out-of-pocket before insurance kicks in) usually lowers your premium. Think of it as betting on yourself – if you're confident you won't need to file a claim, a higher deductible can save you money. Similarly, the coverage limits you select will impact your premium. More coverage generally comes with a higher cost, but also more peace of mind.

So, there you have it! A whirlwind tour of the factors insurers consider. It's not about them trying to trick you; it's about assessing risk and pricing policies fairly.

Remember: Understanding these factors empowers you to make informed decisions about your insurance needs. Compare quotes, shop around, and don't be afraid to ask questions! Knowledge is power, and in this case, it can also save you money.

Feeling inspired to learn more? Awesome! Dive deeper into the world of insurance, research different policy types, and become a savvy insurance consumer. The more you know, the better equipped you'll be to protect yourself and your loved ones. Go forth and conquer the insurance world! (Okay, maybe just understand it a little better, but you get the idea!).