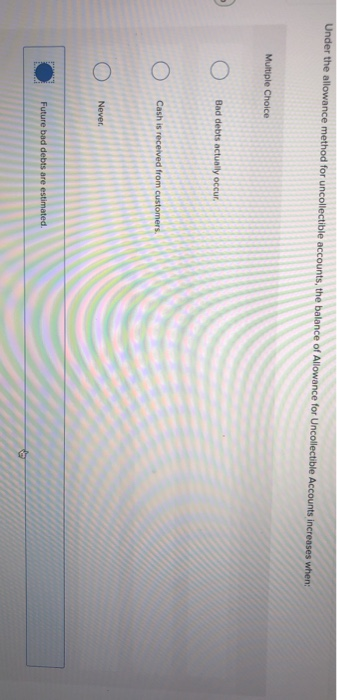

Under The Allowance Method Of Accounting For Uncollectible Accounts

Let's talk about money, specifically, the kind you hope to get! Running a business is all about making sales, but what happens when a customer can't, or just doesn't, pay? It sounds like a downer, but don't worry! We're going to explore a clever accounting technique called the Allowance Method for uncollectible accounts. Think of it as financial planning for the occasional deadbeat – fun, right? Okay, maybe not fun, but definitely useful for a healthier business!

So, what's the big idea? The Allowance Method is all about anticipating that some of your accounts receivable (money owed to you by customers) won't be paid. Instead of waiting until you know a customer isn't going to pay, you estimate the amount of bad debt and set aside an "allowance" for it. This allowance sits on your balance sheet, a little financial cushion for when those invoices go unpaid.

Why go to all this trouble? Well, there are several compelling benefits. First, it provides a more realistic picture of your company's financial health. Instead of pretending that all your receivables will eventually turn into cash, you acknowledge the possibility of losses. This makes your financial statements more accurate and reliable for investors, lenders, and even your own internal decision-making.

Must Read

Second, the Allowance Method adheres to the matching principle. This principle states that expenses should be recognized in the same period as the revenues they helped generate. Since you made the sale (revenue) and extended credit (potential for bad debt) in the same period, it makes sense to recognize the estimated bad debt expense in that same period. It's all about keeping things tidy and logical.

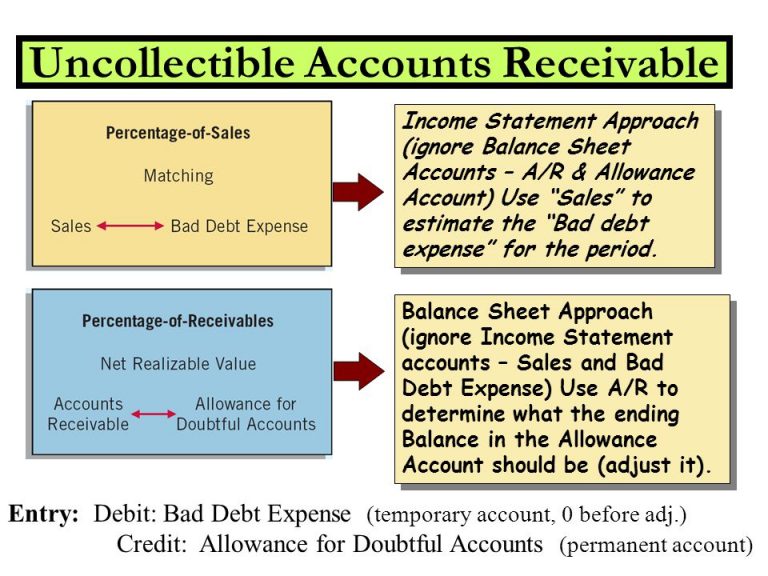

How does it actually work? There are a few common methods for estimating uncollectible accounts. One is the percentage of sales method, where you estimate bad debt based on a percentage of your total credit sales. For example, if you have a history of 1% of credit sales going uncollected, you'd set aside 1% of your current credit sales as an allowance. Another method is the aging of accounts receivable, which involves categorizing your receivables based on how long they've been outstanding. Older receivables are considered riskier and get a higher allowance percentage.

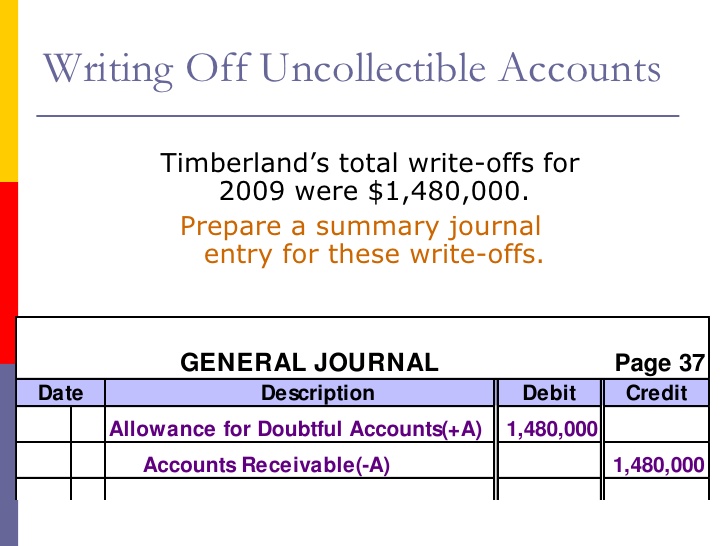

Let's say you estimate $1,000 will be uncollectible. You would then make a journal entry that debits (increases) Bad Debt Expense and credits (increases) Allowance for Doubtful Accounts. This increases your expense and also increases the contra-asset account (Allowance for Doubtful Accounts) that reduces the value of your accounts receivable.

Finally, the Allowance Method helps with tax planning. In many jurisdictions, you can deduct bad debt expense from your taxable income, which can lower your tax liability. However, it's important to consult with a tax professional to ensure you're following the specific rules and regulations in your area.

In conclusion, while dealing with uncollectible accounts isn't exactly a party, the Allowance Method offers a smart and practical way to manage the risk. It provides a more accurate financial picture, aligns with accounting principles, and can even offer tax benefits. So, embrace the Allowance Method and give your business the financial buffer it deserves! Now go forth and collect (as much as possible)!